Stamp duty is a significant cost for Australians looking to buy and move home. To buy a median-priced home, stamp duty costs half a year’s worth of income in Sydney and Melbourne.

Even for more-affordable homes in lower-taxing states, stamp duty costs the equivalent of two months of income.

Read the full report: The Growing Cost of Stamp Duty – PropTrack Report

This wasn’t always the case. Stamp duty relative to incomes is four-and-a-half to six times higher than a generation ago, depending on the state.

While home prices growing faster than incomes is part of the reason why, bracket creep has been a key driver. Nearly all buyers today pay stamp duty equivalent to 3% or more of a property’s purchase price; in the early 1990s as few as 12% did.

This high burden carries real costs for Australia. Joint research undertaken by researchers at the e61 Institute and PropTrack finds that a 1 percentage point increase in the rate of stamp duty reduces the number of home sales by 7.2 percent.

Higher stamp duty makes people less likely to move within their local area or move interstate. This means people are less likely to move for jobs, which may hamper productivity. It also means that stamp duty is among the least-efficient ways to raise revenue.

There are real benefits from reforming stamp duty, but the transition will be challenging. Australia is one of the most-reliant OECD nations on stamp duty, and it is a significant source of revenue for states. Nonetheless, there are ways forward; the ACT and, more recently, Victoria show some of the possible models for transitioning away from stamp duty.

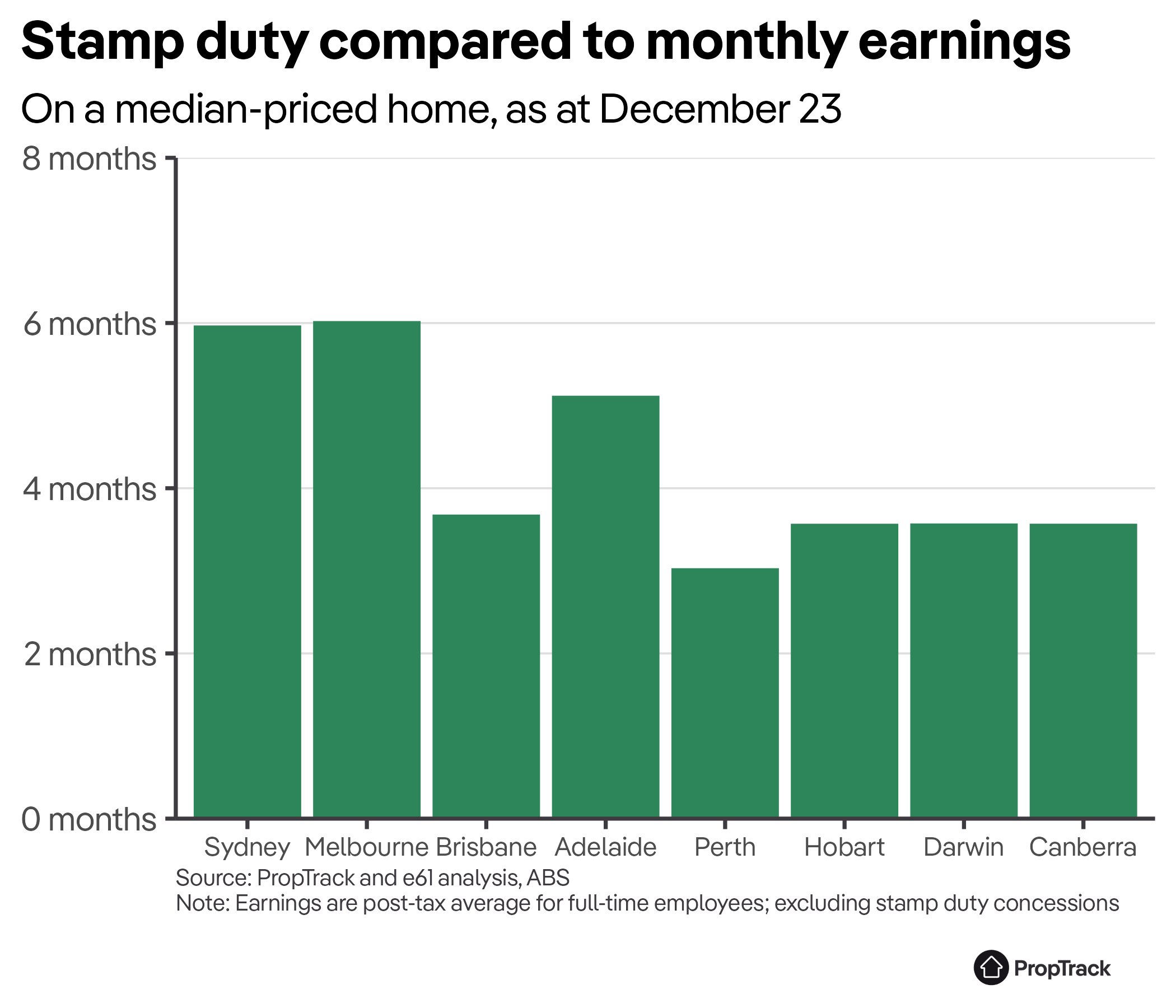

The upfront cost of stamp duty is very significant in every state and territory.

A buyer purchasing a median-priced home in Sydney and Melbourne is looking at paying around $42,000-45,000 in stamp duty – equivalent to about six months of average after-tax full-time wages.

Even in jurisdictions where stamp duty is lower, like Perth, buyers need the equivalent of three months' worth of income to cover stamp duty.

While stamp duty rates across Australia are progressive – meaning buyers pay disproportionately more in stamp duty for more-expensive homes – even buyers looking at more-affordable homes face a large burden.

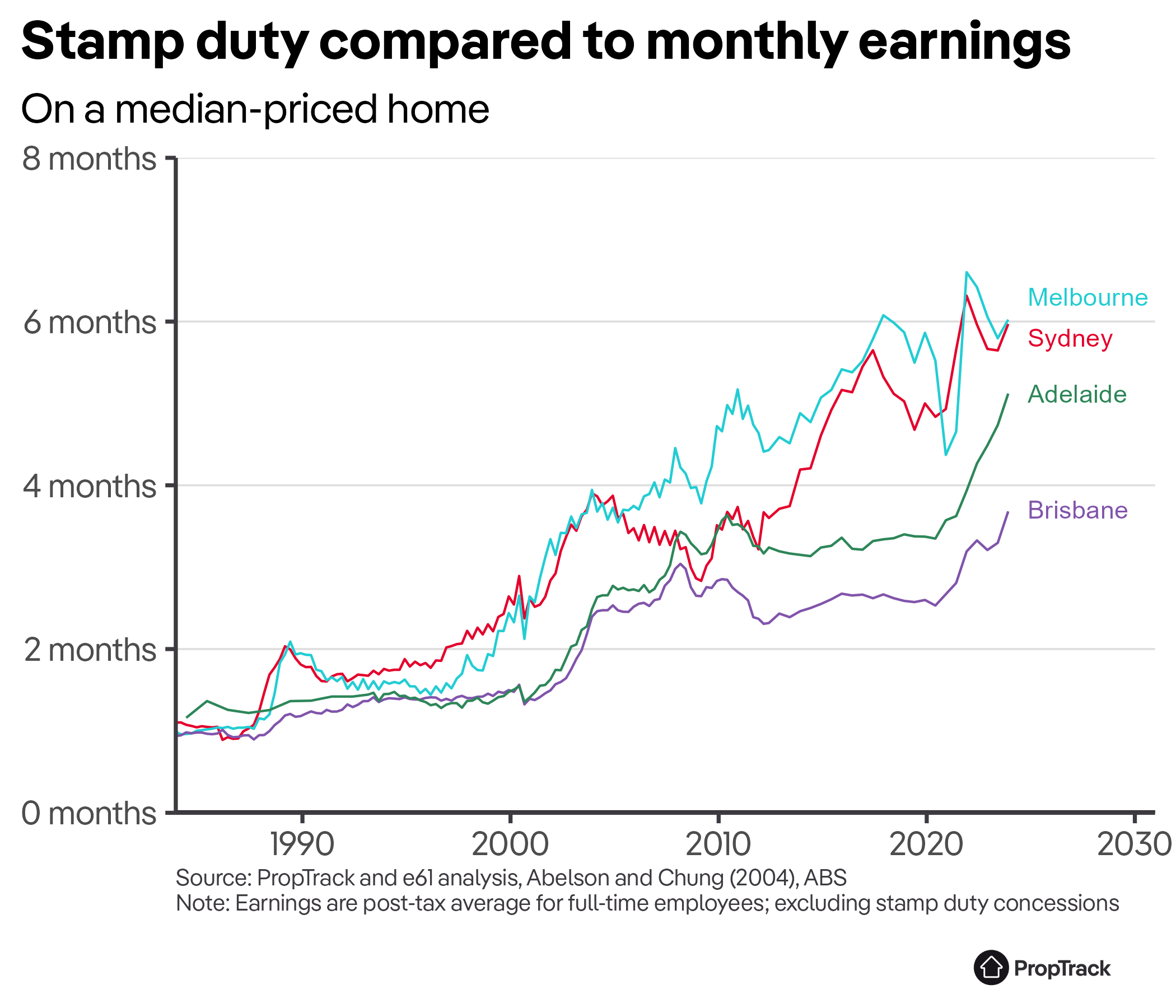

Previous generations of homebuyers did not pay as much stamp duty.

While all states have seen the burden of stamp duty increase compared to prior decades, the increase has been particularly acute in Melbourne.

Compared to the early-to-mid 1980s, a buyer in Melbourne today faces a burden from stamp duty, relative to their income, that is 6.1 times higher.

Stamp duty today is equivalent to 6 months of full-time after-tax income; in 1983 it was less than 1 month.

Similarly in Sydney, someone looking at buying a median-priced home today would pay just under $45,000 in stamp duty – equivalent to six months of income. In 1983 that same buyer would have needed to pay just $1,550, or 1.1 months of income. That represents a 5.4-fold increase.

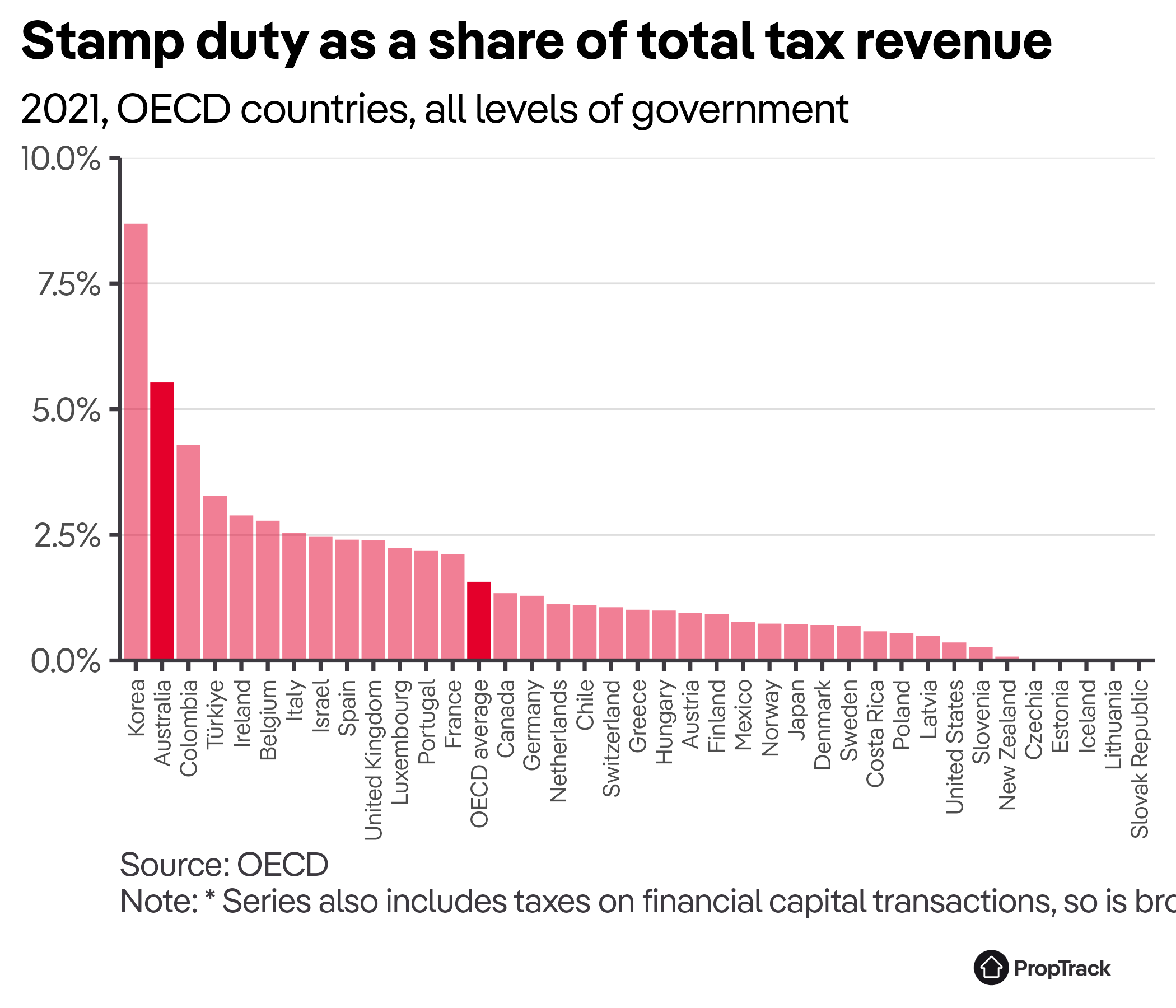

Australia has an unusually high reliance on stamp duty among OECD nations. In 2021, 5.5% of government revenue – across all levels of government – came from stamp duty. That is second only to South Korea.

Comparable nations like Canada (1.3%), the United Kingdom (2.4%) and New Zealand (which does not have stamp duty on residential property transfers) all rely far less on stamp duty to raise government revenue. Across the OECD, around 1.6% of government revenue comes from stamp duty – far below Australia’s 5.5%.

Read the full report: The Growing Cost of Stamp Duty – PropTrack Report

That wasn’t always the case. In the 1970s and early 1980s, Australia’s reliance on stamp duty was much lower – around 2-3% of government revenue – and largely in line with the then OECD average.

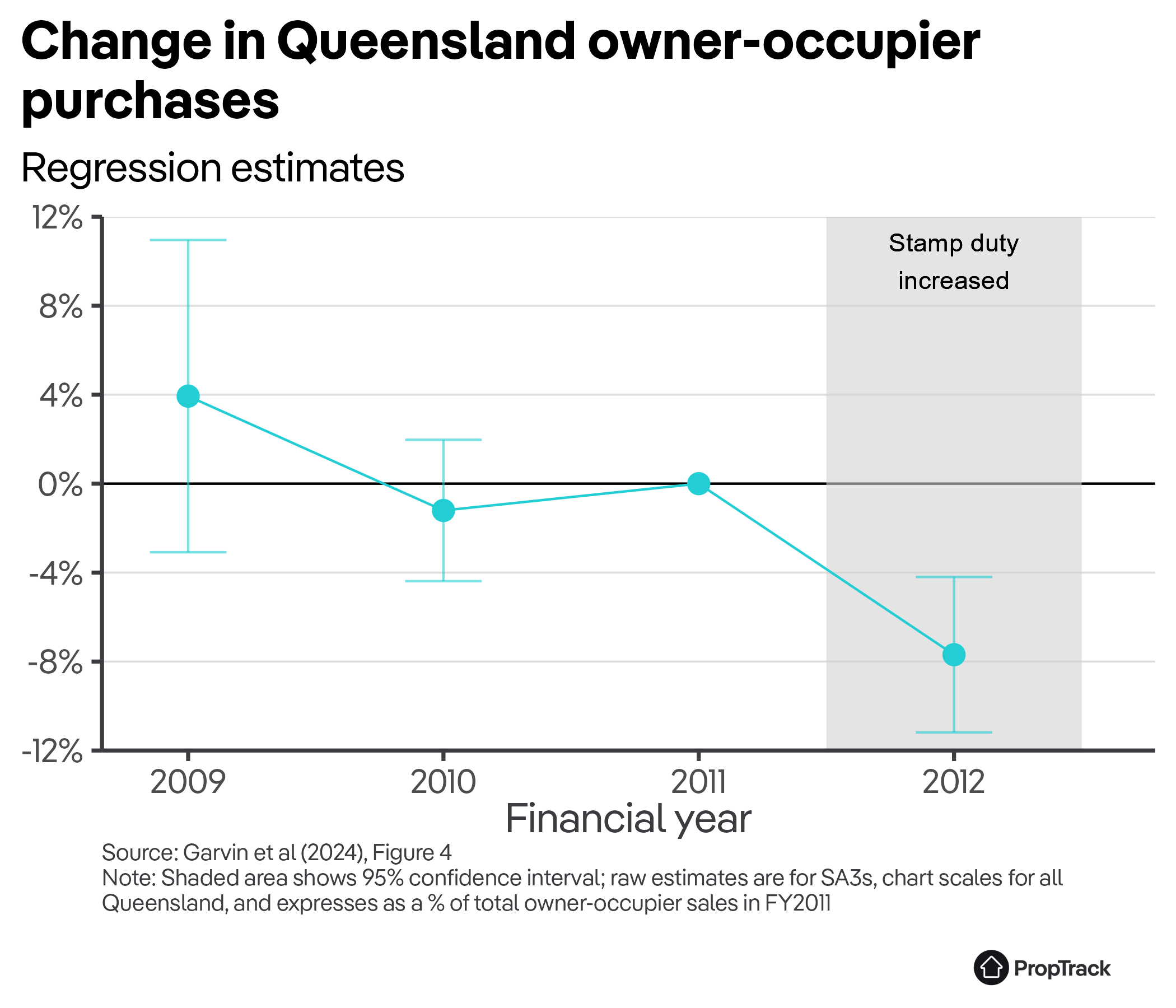

Joint e61 Institute-PropTrack research examines an August 2011 change to the concession for owner-occupiers in Queensland which, on average, doubled the rate of stamp duty that owner-occupiers had to pay (Garvin, La Cava, Moore & Wong 2024).

This change is used as a “natural experiment” to identify the causal effects of stamp duty on housing turnover and how often people move home.

For more detail see the full report: The Growing Burden of Stamp Duty – PropTrack Report

The regression estimates find that the removal of the owner-occupier concession caused 7.7% fewer purchases across the period of the policy change (relative to sales volume in 2011-12). This estimate is statistically significant, and placebo tests support the robustness of the results (Garvin et al 2024, Figure 4).

Accounting for the size of the stamp duty change implies that a 1 percentage point increase in stamp duty (as a share of purchase price) leads to a 7.2% decrease in housing market turnover.

Stamp duty stops people relocating for work and lowers productivity, discourages downsizing and is inefficient way to raise revenue.

The impacts of stamp duty are not confined to the housing market. Making it costly to move homes affects where people live (Garvin et al 2024; Van Ommeren & Van Leuvensteijn 2005), and that could affect the jobs they choose to take and, relatedly, how far they must commute.

Stamp duty discourages older households from downsizing when their house becomes surplus to their needs because it adds tens of thousands of dollars to the cost of doing so.

Because households are quite responsive to the cost of stamp duty, it is an economically costly and inefficient way to raise revenue, compared to many other taxes which do not induce as large a change in households’ choices.

Numerous studies find that stamp duty ranks as one of the least-efficient ways of raising revenue.

For more detail on these impacts, read the full report: The Growing Burden of Stamp Duty – PropTrack Report

Replacing stamp duty with a broader-based land tax would be fairer and more efficient.

Broad-based land taxes are a more efficient way to raise revenue. They are also fairer because they spread the burden of taxation, and, unlike stamp duty, do not differentially tax households of otherwise similar income and wealth simply because one moves home more often.

Replacing stamp duty with land tax is not the only option; stamp duties are among the least efficient ways of raising revenue, so almost any other tax would be an improvement. However, states have few options for raising revenue, which leaves land tax as a natural choice.

While transitioning from stamp duty to land tax is difficult, there are several approaches, outlined in the Henry Tax Review (Treasury 2010): a gradual transition, a ratchet change, and an immediate change with credit past stamp duty paid.

For more detail on these options and how they could be implemented, read the full report: The Growing Burden of Stamp Duty – PropTrack Report

Adopting a gradual transition provides both the simplest and fairest approach to transition away from stamp duty.

By slowly reducing the rate of stamp duty, state governments do not face large short-term revenue shortfalls – unlike a ratchet transition in which up front stamp duty revenues are immediately forgone. And by gradually increasing land tax rates, rather than immediately changing over, homeowners are not faced with unexpected and unplanned-for taxes.

Credit should be provided for recent buyers and for buyers that pay stamp duty during the transition period. This credit would be equal to the stamp duty paid and would offset future land tax obligations. Such a credit would avoid any perceptions of “double taxation” of recent buyers.

For recent buyers, this credit should be pro-rated depending on how long ago they purchased, so as not to provide unnecessary compensation for those that last paid stamp duty some time ago.

State governments should look at undertaking this transition over a five-to-ten-year period, so as to benefit from the abolition of stamp duty sooner and to minimise risks of the reform being abandoned.

For retiree, asset-rich but low-income households, for whom annual property tax could be a substantial impost, a deferral scheme should be available that would allow property tax obligations to accumulate and be discharged on the sale of the property.

For more detail on these options and how they could be implemented, read the full report: The Growing Burden of Stamp Duty – PropTrack Report