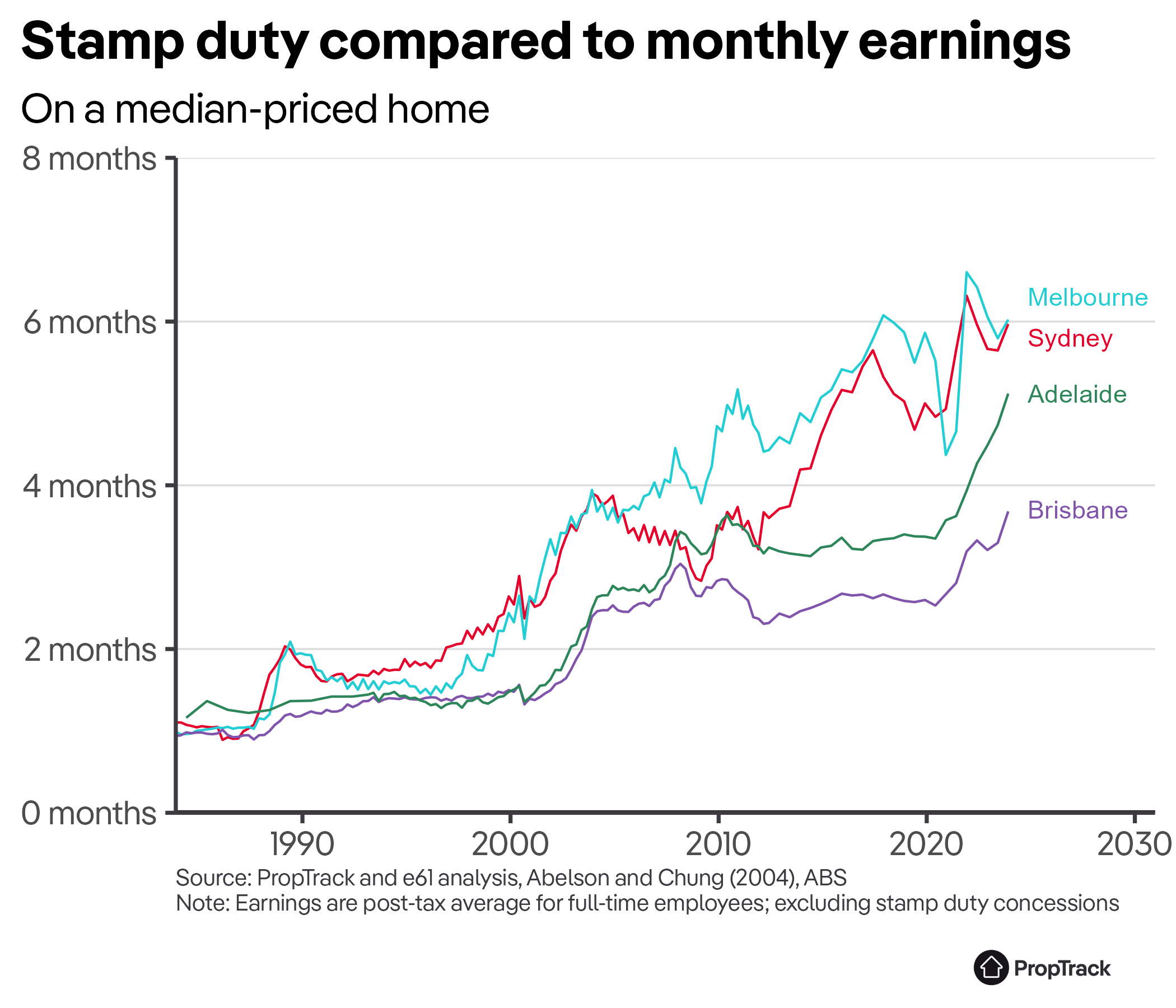

A buyer in Melbourne today is paying 6.1 times as much stamp duty, relative to their income, as a buyer in the early 1980s to buy a median-priced home.

And while Melbourne has seen the largest increase, it’s far from alone – buyers in other cities are paying between 4.4 and 6 times as much stamp duty as previous generations.

There are two reasons why today’s buyers pay so much more stamp duty.

First, home prices have grown faster than incomes. Between the early 1980s and today, median home prices have increased two-to-three times faster than incomes. That means that stamp duty has also increased faster than incomes.

That’s an important part of the story, but it only explains about half – or even less in some states – of the increase in stamp duty.

The other big driver is bracket creep.

Bracket creep happens because stamp duty rates are progressive – more expensive properties pay a higher rate of stamp duty.

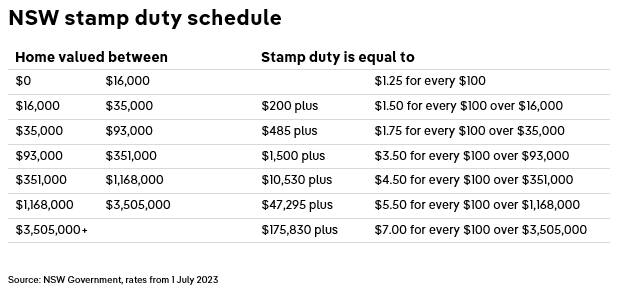

For instance, NSW has a series of seven brackets for stamp duty, shown in the table below.

Each bracket pays stamp duty equal to the amount that a home just below the bracket pays, plus a higher 'marginal rate' for every dollar the purchase price exceeds the bracket threshold. These marginal rates get higher with each successive dollar.

This structure of higher marginal rates kicking in as the sale price crosses a particular threshold means that average tax rates - the stamp duty paid divided by the purchase price - increase as the price increases.

This is the same way income taxes work – higher marginal rates apply to earnings above certain thresholds, which means as you earn more income you pay a higher average tax rate.

Other states have similarly progressive scales, where higher marginal rates of stamp duty apply as homes reach certain price thresholds.

Bracket creep happens firstly because the price brackets have been updated only infrequently, and secondly because home prices have grown, often substantially, since the brackets were last set.

That means more properties have moved up the brackets and are now paying higher rates of stamp duty.

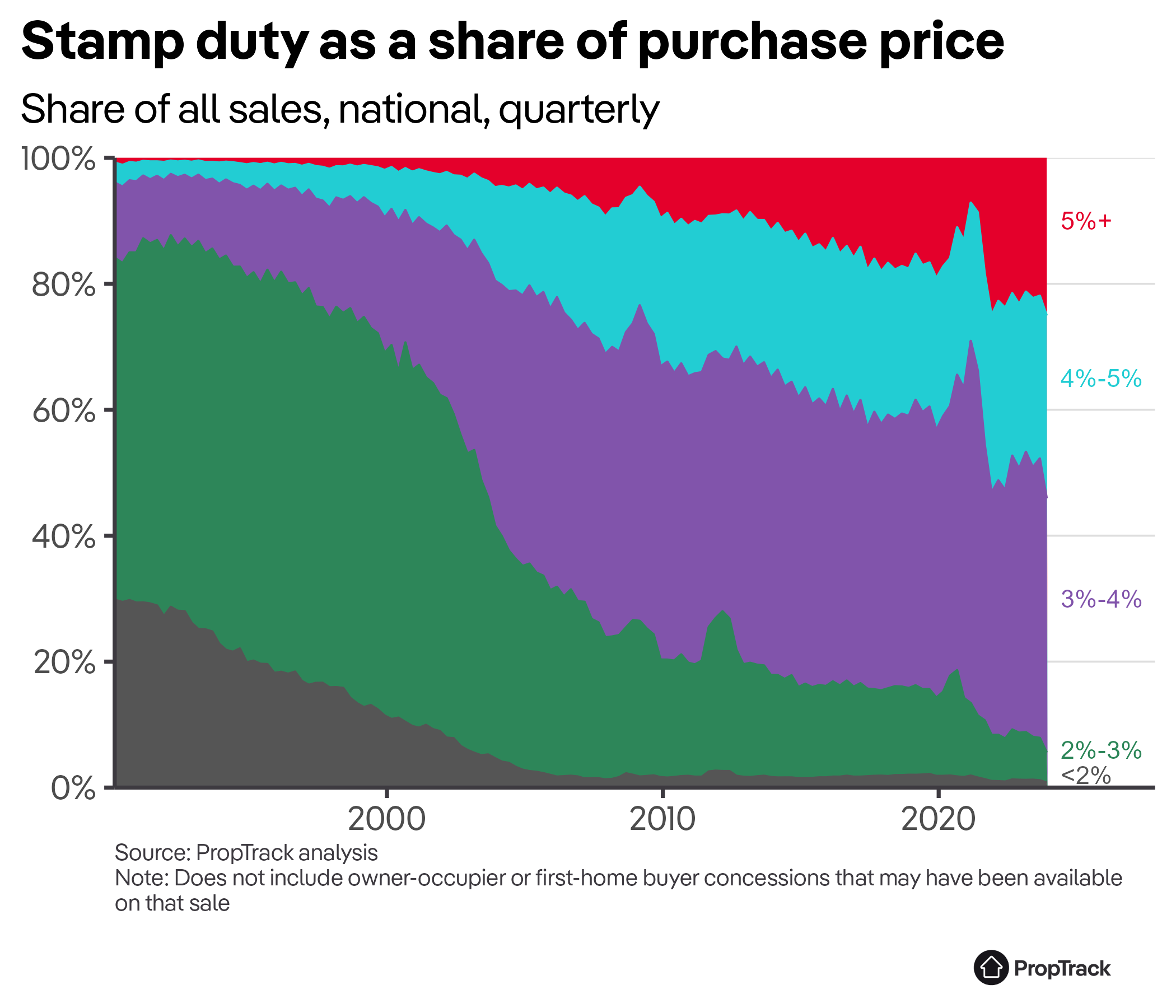

The result of this process of bracket creep is that almost all transactions in 2023 faced a stamp duty rate equivalent to 3% or more of sale price, and one-in-five paid more than 5%.

That share has increased substantially over the past few decades. In the early 1990s, it wasn’t uncommon to pay stamp duty of less than 2% of purchase price, and nine in ten sales paid less than 3%.

While all states have seen increases in the average stamp duty rate for a median-priced home, it is particularly acute in Melbourne. A buyer today is paying stamp duty equivalent to about 5.4% of purchase price; in the early 1980s, a buyer of a median-priced home would have paid stamp duty of about 2% of purchase price.

While Melbourne is the starkest increase, the story is similar elsewhere: a median-priced Sydney home today faces stamp duty equivalent to a little over 4% of purchase price versus 2% in the early 1980s.

A Brisbane owner-occupier has gone from paying stamp duty equivalent to 1% of purchase price to 2.6%, and in Adelaide from 2.5% to 4.6%.

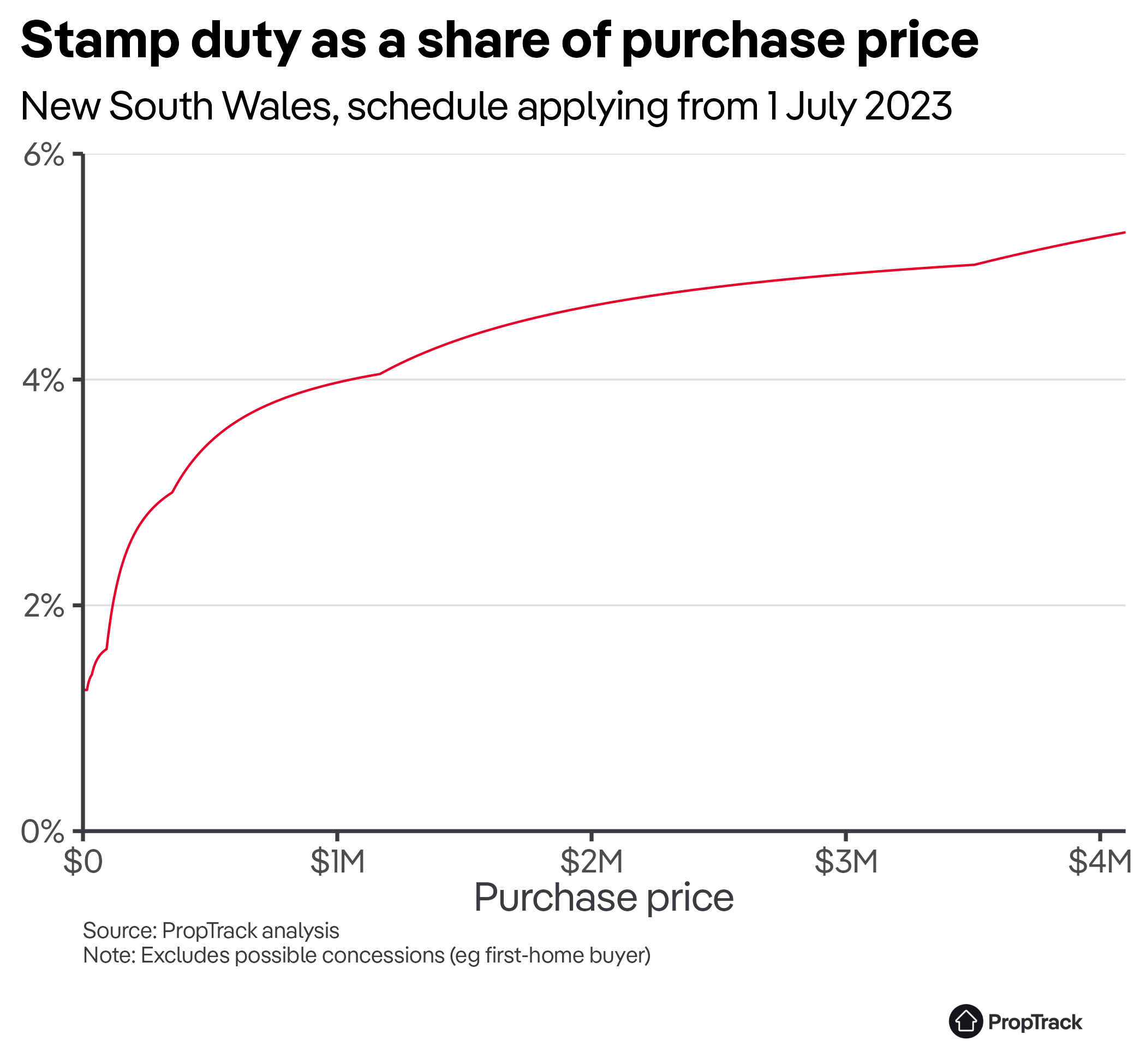

Not all of the increase in stamp duty is due to bracket creep – some states have made policy changes to increase stamp duty rates, mostly by adding higher-marginal-rate premium brackets.

Notably, NSW added a $3 million plus rate in 2004, which has since been moved up to $3.505 million; Victoria added a $2 million plus bracket in 2021.

But bracket creep has been, far and away, the main contributor and means today’s buyers are paying much more stamp duty – not just relative to their income, but also relative to the price of their home.