While there have already been some signs of slowing price growth over recent months, prices are still rising. But can it continue?

The Reserve Bank of Australia's November rate hike will put further pressure on households, squeezing borrowing capacities and increasing mortgage servicing costs.

An uplift in property listings during spring has also shifted dynamics in some markets.

With the selling season in full swing, activity has picked up and October was the busiest month for auctions so far this year. Last week's rate rise could also affect the outlook, depending on the RBA’s next move.

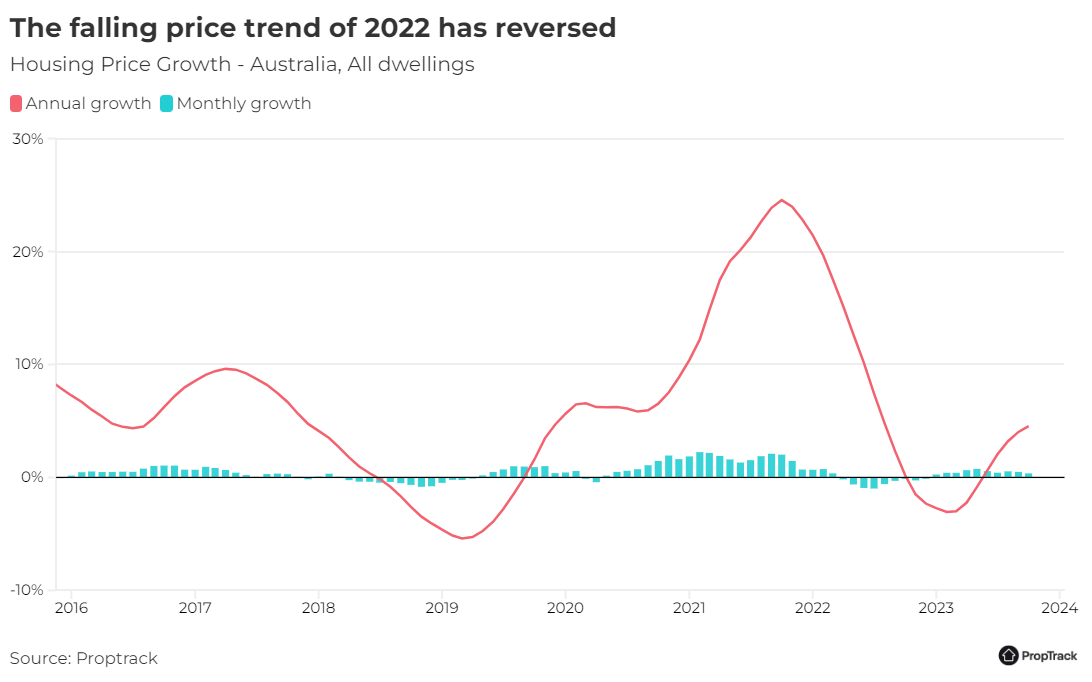

The latest PropTrack Home Price Index shows many markets have recovered last year’s fast falls entirely and are now in the midst of a fresh upswing.

For national home prices, the 10 straight months of gains is the longest stretch of growth since the pandemic boom when prices rose for 23 straight months after very small falls in March and April 2020.

In the first half of this year the turnaround in home prices was underpinned by the subdued listings environment that meant buyers were competing for fewer properties.

While stronger housing demand was also a factor, population growth has been an important tailwind, alongside tight rental markets and wages growth slowly increasing with the unemployment rate at multi-decade lows.

Significant home equity gains for existing homeowners are also likely to have buoyed upgrader activity, making these buyers less affected by rate hikes.

However, dynamics have shifted in recent months, especially in Sydney and Melbourne with a significant uplift in number of properties hitting the market.

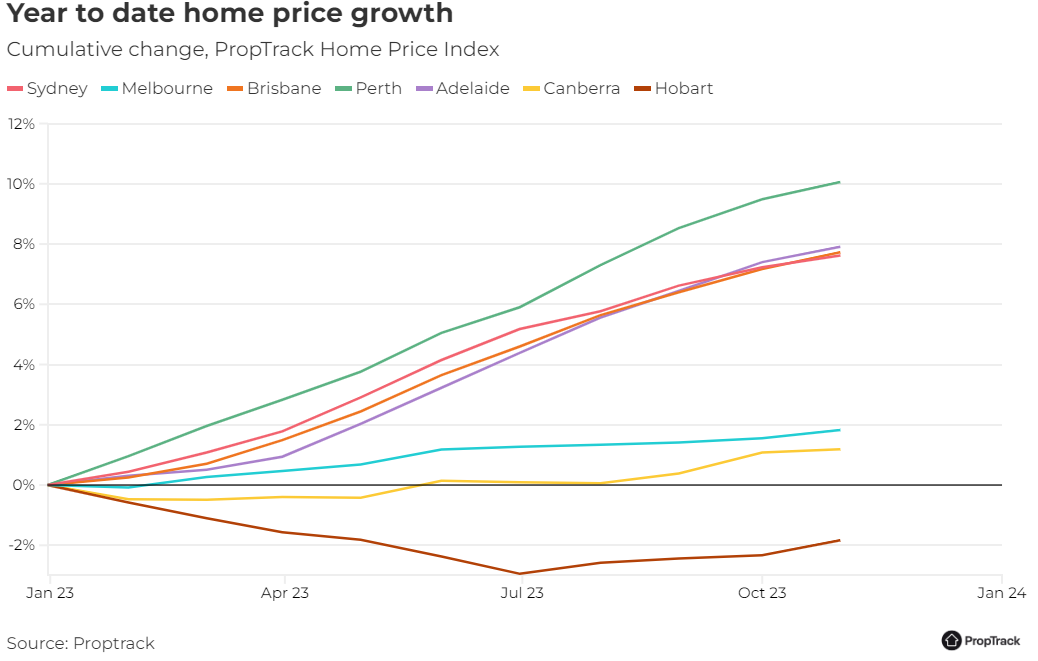

The picture remains a little different in other markets. Choice for buyers remains limited in Brisbane, Adelaide, and Perth, heightening competition and pushing prices to fresh peaks in each of these markets in October.

Despite the uplift in new listings volumes, the price recovery has continued, and prices moved higher in every capital city except Darwin in October.

Nationally, the number of enquiries per for sale listing increased 19% year-on-year in October but remains below the record high levels seen in late 2021. This shows that although the flow of new listings hitting the market has risen with the selling season underway, housing demand has remained strong.

The number of enquiries per for sale listing is also up in Sydney (+16% year-on-year) and Melbourne (+10% year-on-year), with the bigger lift in new listings hitting the market giving buyers a lot more choice than earlier in the year and easing competition.

In Perth, Adelaide and Brisbane where conditions are more competitive, the number of enquiries per for sale listing is up 107%, 24% and 57% year-on-year in October respectively.

Shortages of skilled labour, materials and higher costs have constrained the home building industry and slowed the completion of new homes, fueling a housing shortfall.

This shortage of new builds is also contributing to the lift in prices so far this year amid strong demand for housing stemming from rapid population growth, low unemployment, a decline in average household sizes and tight rental markets driving people towards buying.

With population growth surging and average household sizes still smaller than before the pandemic, we need to be building more housing.

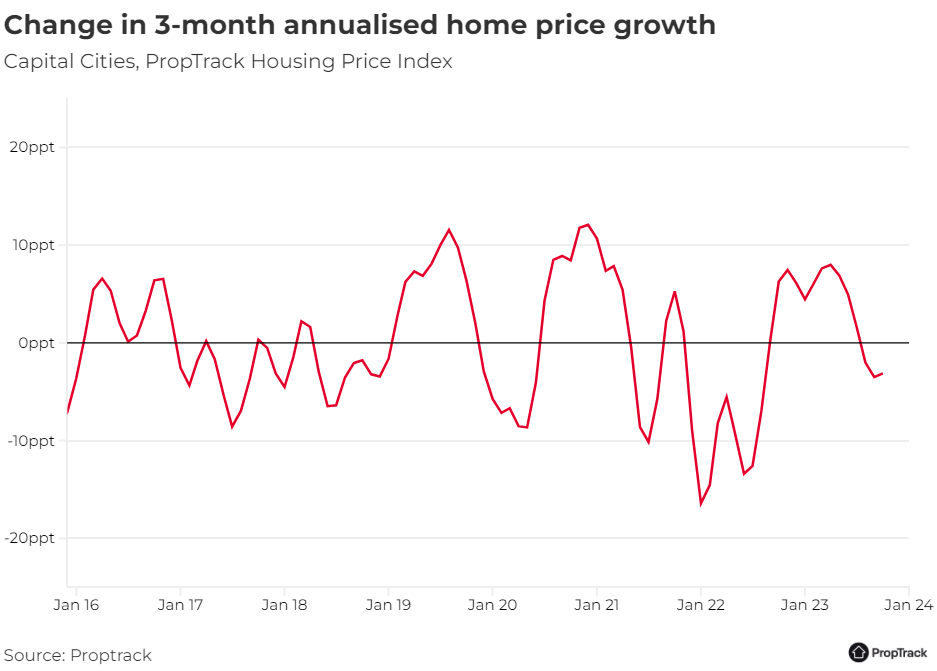

Annualised six-month ended price growth in the capital cities is still 4 percentage points higher than six months ago, showing the momentum in home price growth remains stronger than early in the year when the recovery was first underway.

However, comparing three-month periods, the pace of home price growth does appear to be slowing from the faster pace recorded in May, June, and July in some capital city markets.

The October Home Price Index shows annualised three-month ended price growth in Sydney, Brisbane, Perth, and Adelaide is lower than the three months prior, however these cities still have the strongest growth of the capitals despite slowing.

The slowdown in growth is fastest in Adelaide, where annualised three-month ended price growth is 5.4 percentage points lower than in July this year.

In Hobart and Canberra, where the recovery has lagged, the pace of growth is accelerating.

The uplift in the number of properties coming to market is likely one factor that has eased the pace of growth in Sydney.

But although the flow of new listings hitting the market in Brisbane, Adelaide, and Perth has increased from the winter months, it has remained relatively subdued, and the total number of properties listed for sale remains below historic averages.

The curtailing of the pace of growth is not necessarily surprising, given the rapid turnaround in prices earlier this year, a higher volume of listings and affordability constraints in play. This is typical of phases of growth – the upturn begins, accelerates, and plateaus.

Prices in Perth have been on the rise for 42 straight months, while Adelaide prices have risen for 40 months, with the exception of small falls in both cities in June 2022.

Home price growth remains above historic average growth in Sydney, while in Brisbane, Adelaide, and Perth, prices are growing at more than double the historic average annual pace of growth.

In the regions, and in Melbourne, Hobart, and Canberra the pace of price growth is accelerating after lagging the recovery in Sydney and Brisbane and continued upswing in Perth and Adelaide for much of this year.

This highlights the variance in conditions and market dynamics across the different cities and regional markets.

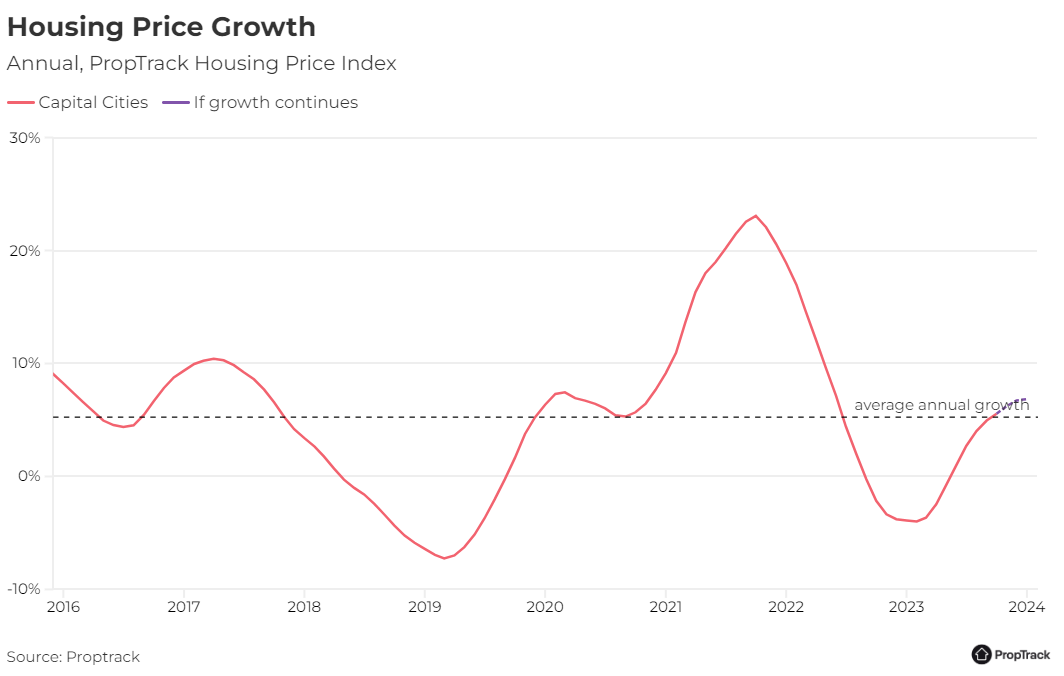

Despite the pace of growth beginning to slow in some parts of the country, further growth is expected ahead, albeit at a slower pace.

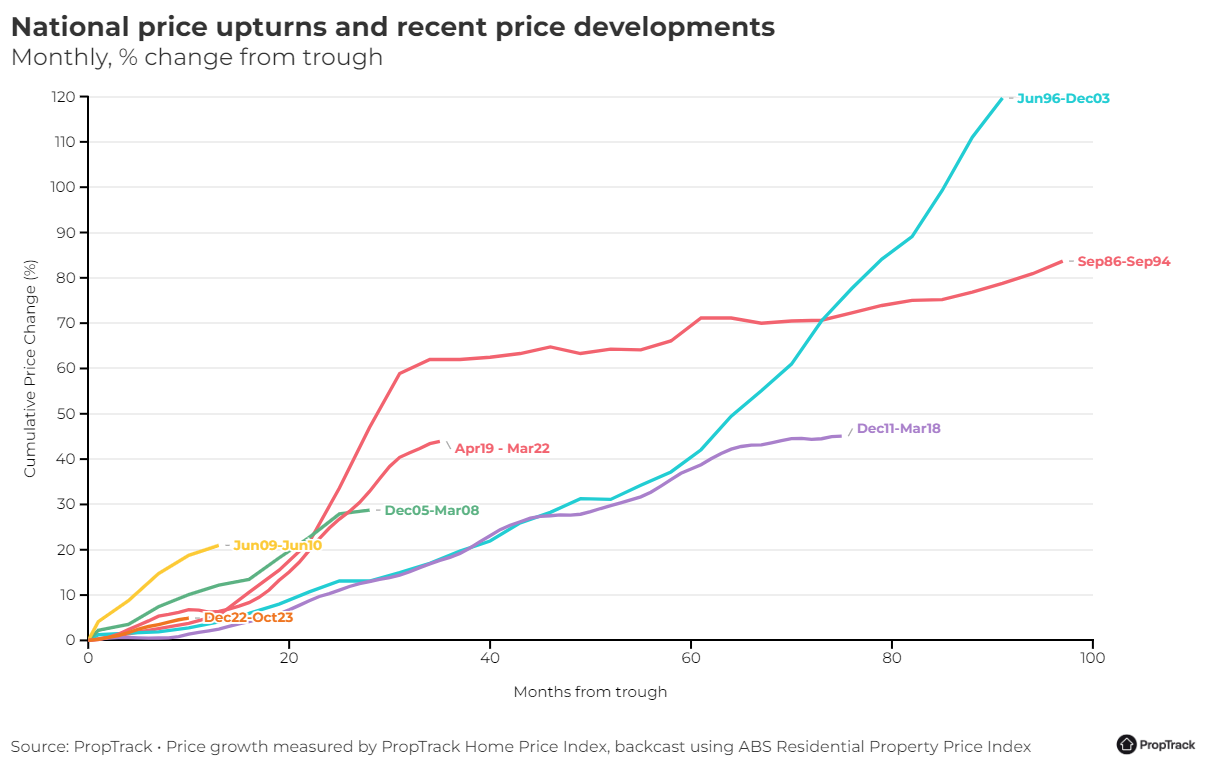

Looking at previous upturns can provide context and understanding of long run changes in home prices.

Although there have been six national downturns of note since 1990, prices have spent much longer rising than falling.

This additional increase in interest rates is likely to further slow the pace of home price growth. Affordability remains stretched and is set to remain so into 2024, with the economy expected to continue slowing.

But unless interest rates move significantly higher from here, population growth, tight rental markets, and a slowdown in the completion of new builds will likely continue to buffer the impact of monetary tightening.

There is a risk that interest rates move higher again. Inflation pressures are trending lower, but this is happening slower than expected. Continued increases would be a risk factor for current dynamics.

Looking ahead, though the pace of price growth is expected to continue slowing, home prices in 2024 will also be influenced by whether interest rates begin to move lower.

Some expect rates will stay high for some time, but many expect interest rates will be cut at some point in the second half of 2024, causing borrowing capacities to increase and mortgage servicing costs to decrease, likely fueling continued growth with housing supply set to remain constrained.