Australia is in the midst of a population boom, driven by a surge in net migration following pandemic border closures. But with record low vacancy rates and deteriorating affordability, will we be able to house everyone?

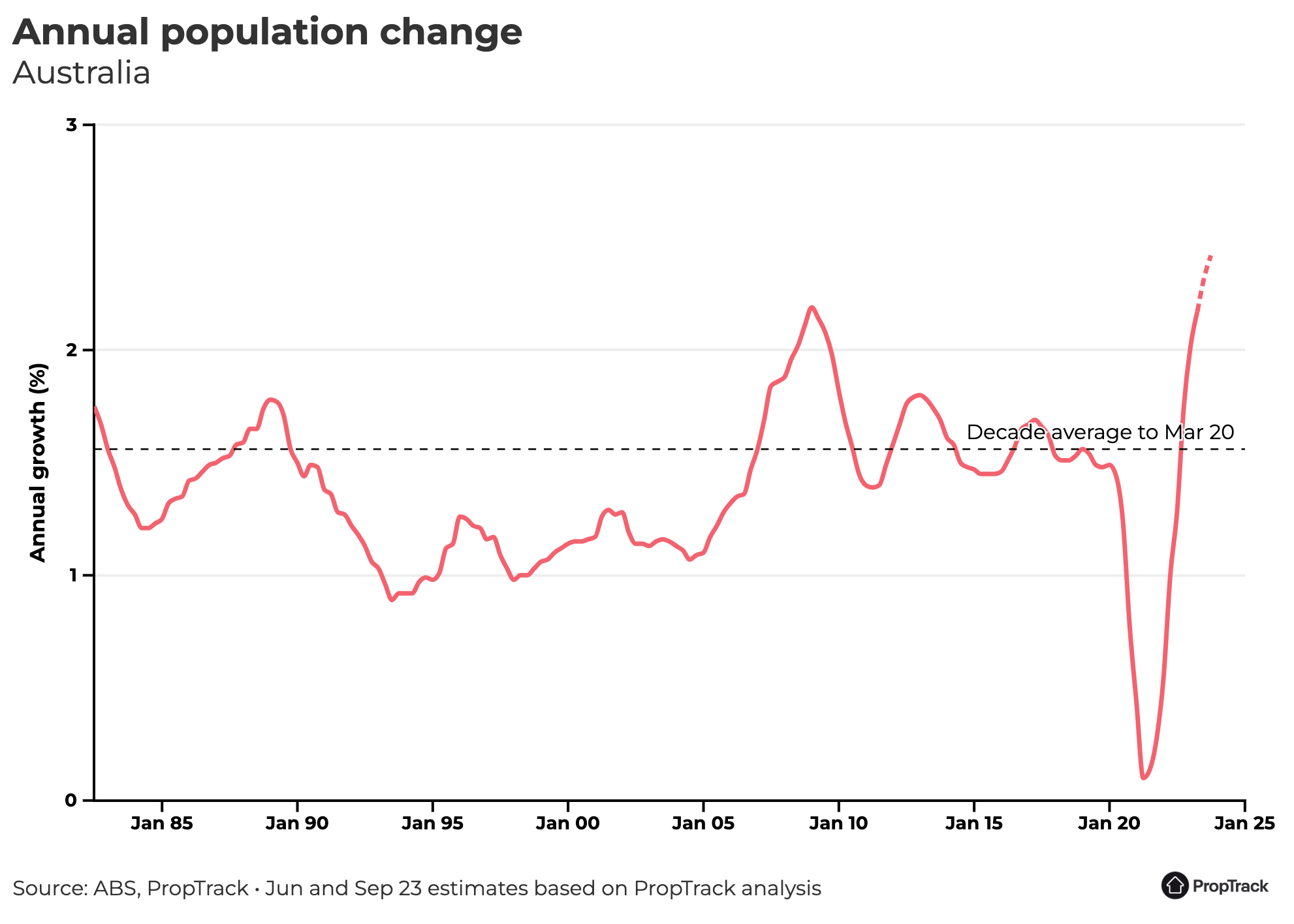

In 2022 the population grew by record numbers – the largest ever recorded numeric increase in a calendar year according to the Australian Bureau of Statistics (ABS).

This growth is now continuing into 2023. In fact, it's accelerating.

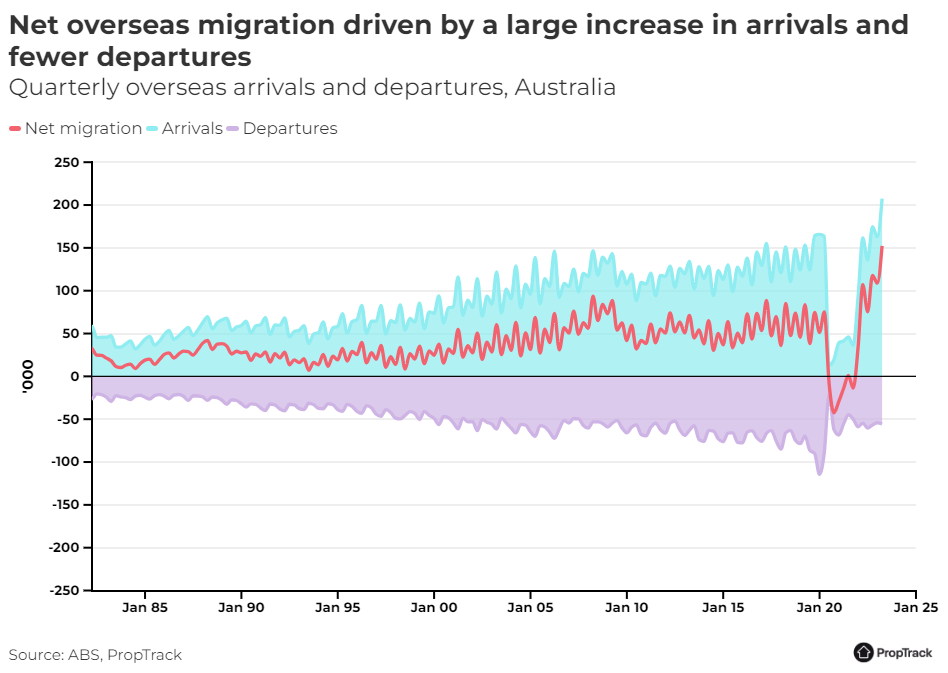

ABS data revealed the highest national quarterly population increase on record in the March quarter, with the gains from migration having never been higher.

The increase was mostly through net overseas migration of 454,400 people, with fewer departures and a high rate of arrivals, equating to around 182,000 additional households.

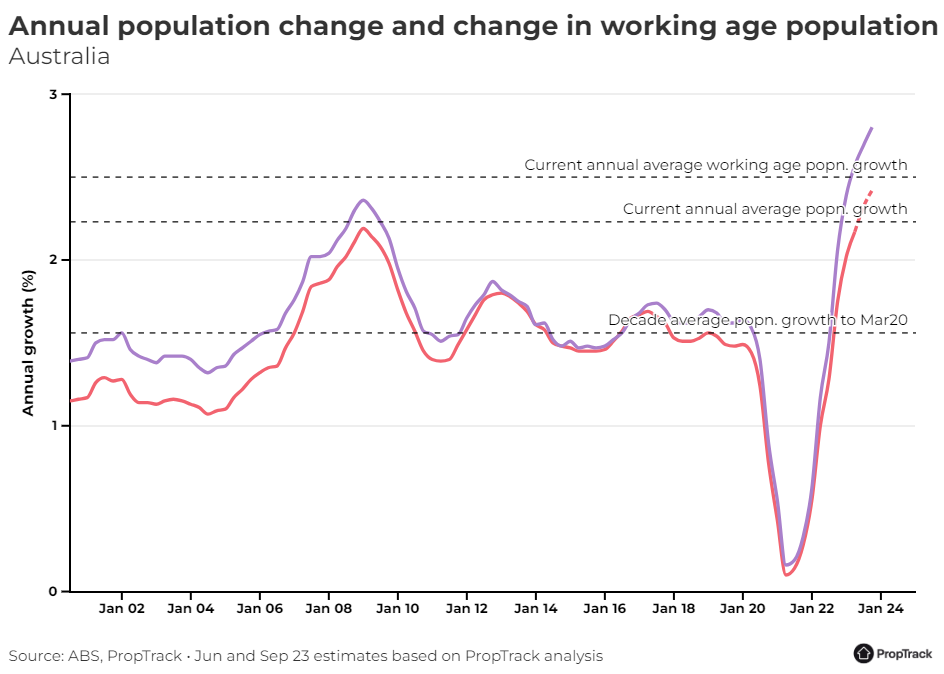

While the official data is not particularly timely, there are many indications that the strong population growth has continued - and accelerated - to even reach new historic records.

Net long-term and permanent arrivals are a timelier proxy for the official data and indicate continued strong net migration gains in the June quarter and beyond.

Based on this, overall annual growth could clock another record of just north of 600,000 persons, assuming the natural increase projections in the 2023–24 Budget.

These estimates driven by net migration gains are well above those forecast by the government in the latest Federal Budget.

Comparing migration gains to the average in the decade to March 2020 prior to the pandemic, shows an additional uplift of ~190,000 in 2022, and possible lift of ~300,000 in 2023, meaning net migration will have fully caught up the pandemic losses (~440,000) and will be ~50,000 additional by the end of this year.

These excess gains are expected to begin easing in 2024 and 2025, but are likely to remain elevated in comparison to the pre-pandemic trend, adding to demand for housing.

Even now, search data shows the interest in Australian property from overseas has never been higher.

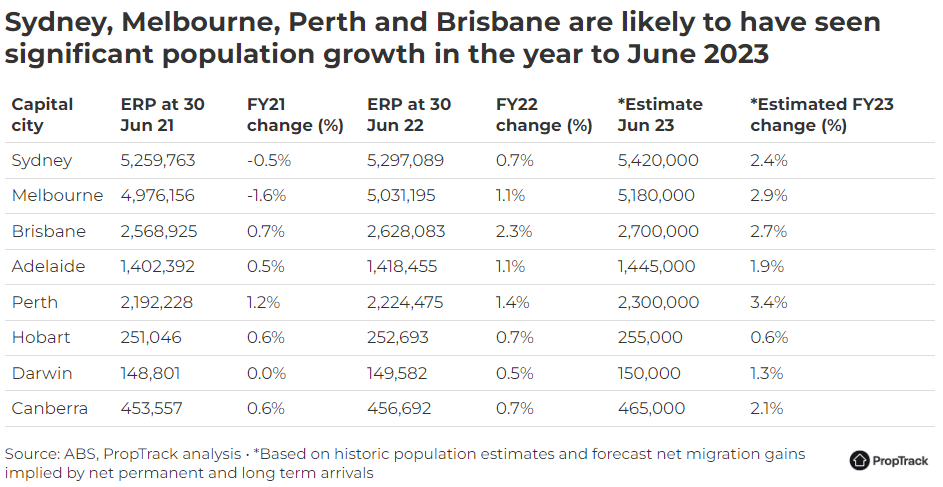

Capital city estimated residential population (ERP) updates are even less timely, but using historic average shares to estimate potential population gains at the capital city level indicates potentially a very fast pace of growth in some cities.

While not a perfect measure (given factors such as Covid have affected the number of Australians moving interstate) we can roughly estimate that Sydney, Melbourne, Perth and Brisbane are likely to have seen significant population growth in the year to June 2023.

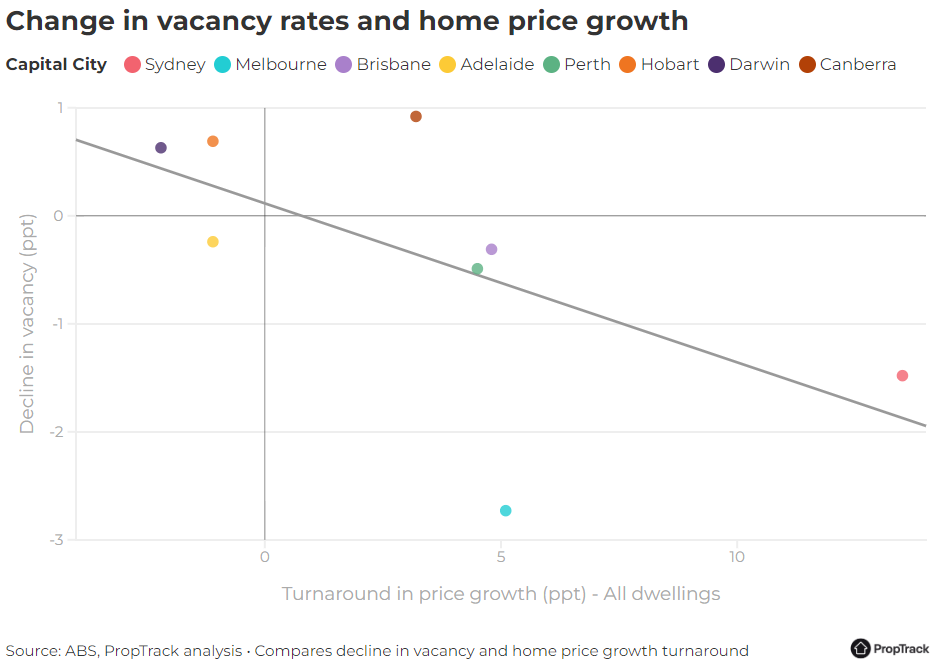

This has likely contributed to the fast turnaround in home prices seen in 2023, alongside tight rental markets.

The reversal in price growth has been most significant in markets where population growth has picked up the most and rental markets have tightened most.

However, though a contributor, the causality between population growth and home price growth isn’t that simple in reality, and other factors like supply conditions matter greatly.

So how much has resurgent population growth added to housing demand? With net migration expected to catch up and outpace pandemic losses this year has this impacted housing demand?

Smaller household sizes during the pandemic resulted in significant additional demand for housing and roughly offset the entire lost population increase across both 2020 and 2021 combined.

Although recent data suggests that average household sizes (AHS) have begun to increase in the capital cities in recent months, the AHS remains below pre-pandemic levels and was at a historically low 2.49 people per household in January 2023.

And now net migration will has fully caught up the pandemic losses and then some, meaning demand for housing is much stronger.

While growth is expected to ease in 2024 and 2025, against the backdrop of pre-existing housing supply issues, faster than expected population growth has meant more people are calling Australia home, giving rise to a mismatch between housing supply and demand.

An additional factor, given that more than 80% of population growth is currently stemming from net migration – that growth means more working-age adults than it would if growth stemmed from natural increase. This means that growth in the adult population is steadily higher than total population growth further boosting demand for housing.

Using the official population change in the year to March 2023 a potential 226,000 additional households would have needed homes. Australia completed around 170,000 new homes over the year to March 2023, meaning a shortfall of around 56,000 homes based on population growth alone.

This is a problem, with supply already limited and smaller households having already compensated the missing population gains in 2020 and 2021. Meaning the strong rebound in migration and “excess” growth face fewer options, clearly identifying the requirement to address our housing shortage.

Using the growth estimates for the 6 months following March 2023, indicate that unless the pace of building activity steps up a further 41,000 shortfall would be incurred. Obviously, not all of our growing population would be housed in new homes, with the rental market, and existing dwellings also being housing options and recent arrivals to Australia historically being most likely to rent.

But this does serve to illustrate a point that with the current housing shortage and immediate supply issues, challenged rental market conditions and the worst affordability in at least three decades – these issues aren’t likely to be improving.

With population growth likely to place continued upward pressure on home and rental prices whilst supply conditions remain constrained.

Governments have begun to recognise the need for more housing, and in August, the National Cabinet agreed to build 1.2 million homes over the next five years.

Currently, we're not building enough to hit that goal. To meet the 1.2 million goal, we need to increase our pace of building by almost 40% from where it currently stands.

And concerningly, based on current estimated annual growth of close to 600,000+ people per year (both natural increase and net overseas migration), the new residents will simply absorb the 1.2 million homes based on an AHS of 2.49.

Mitigating factors here are the potential for household sizes to increase, population gains to slow more markedly into 2024 and beyond, and building activity recovering.

As the population continues to grow, more action on housing supply will be required as well as infrastructure and investment frameworks to maintain the liveability of our future cities.

A combination of fast-tracking new supply of more of the right type of homes built where people want to live, more medium-and high-density development, as well as policies that reduce the planning impediments that hinder new supply and encourage better use of existing homes can help ease constraints.