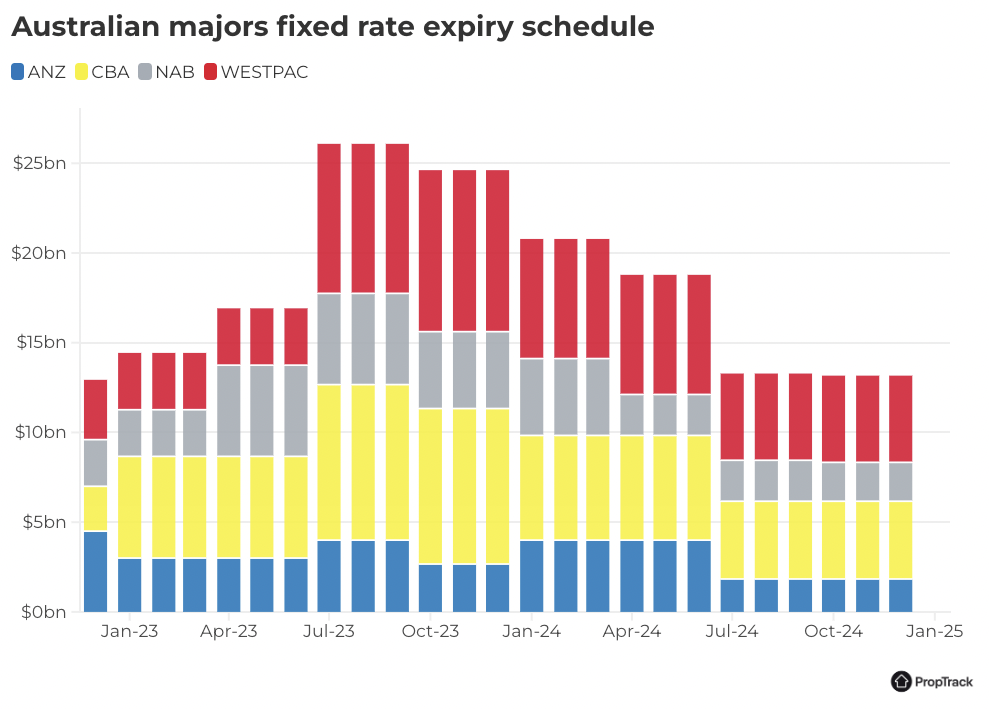

With only four months remaining of the year, the ‘fixed-rate cliff’ as has been colloquially termed is passing the halfway point, with more than $100 billion in fixed rate mortgages set to expire by the end of the year.

After a 400-basis point increase in interest rates across 12 step changes, we take stock of what’s on the precipice of the so-called cliff.

Firstly, who’s at risk? Just over a third of Australian households have a mortgage (35%). The remaining just under two-thirds are divided evenly between renters (31%) and homeowners without a mortgage (32%), The latter collective clearly doesn’t have to worry about the impact of significantly increased mortgage servicing costs.

Fixed rate borrowing increased significantly during the pandemic when the RBA’s term funding facility allowed banks to offer ultra-cheap fixed rate mortgages.

Many borrowers took advantage of these historically low fixed mortgage rates, with the fixed share of outstanding loans almost doubling to about 40%, although variable-rate loans still retained the majority.

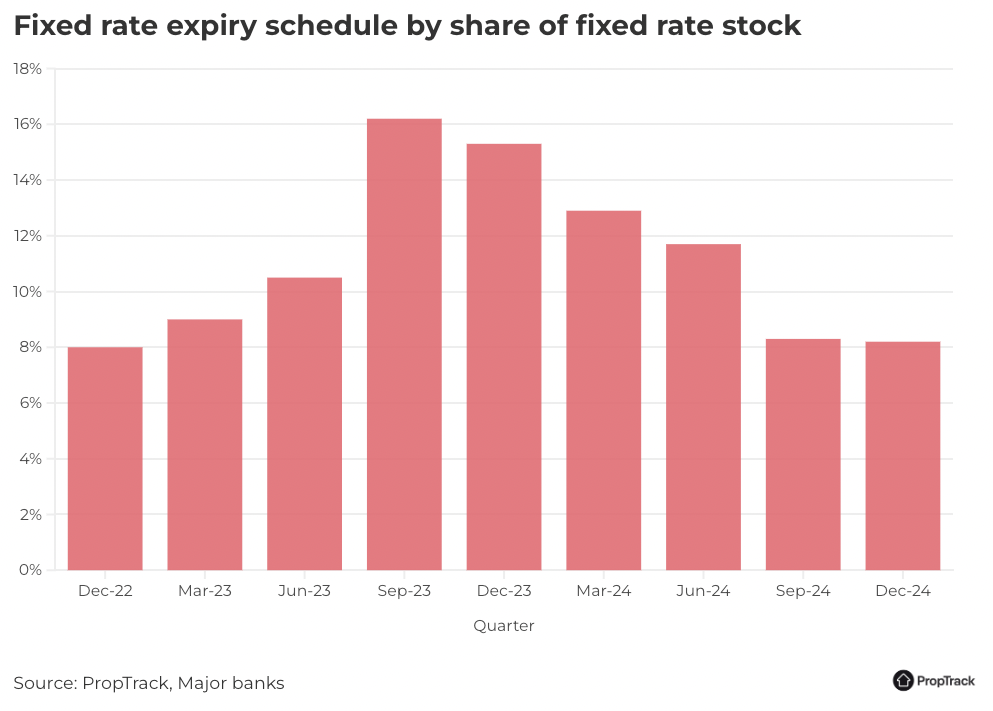

RBA analysis estimated that about 880,000 fixed-rate loans would expire in 2023.

Most of these expiries are occurring in the second half of 2023. Borrowers with expiring fixed-rate loans face sharp increases in their repayments. Exactly how much depends on the original fixed rate, the timing of expiry and ability to refinance with a different lender (most lenders offer new customers their most competitive rates) but most will see repayments increase by a minimum of 30%.

Though this process has been ongoing throughout the year, we are now at the peak of the fixed rate cliff now. With the bulk of this expiry occurring across July, August and September, close to $30bn in fixed rate loans will expire each month across the four major lenders.

There are promising signs that this process, while no doubt challenging for many households, has not yet and will likely not bring the deluge of forced sales that some have forecast.

Household finances are supported by the strong labour market conditions with the unemployment rate holding close to multi-decade lows and wages growth slowly increasing.

The much larger cohort of borrowers on variable rates have already endured the tightening that has been passed through to date without a visible increase in distressed sales or mortgage arrears.

There’s no denying that the fastest tightening cycle in a generation has had an impact on households, with mortgage payments as a share of household disposable income having increased to historic levels. No doubt many households have been forced and will continue to make substantial budgetary adjustments as the share of fixed rate expiries accelerates, but mortgage holders tend to prioritise repayments and dial back discretionary spending over selling their home.

Consumer spending has slowed materially and is expected to continue to do so as the substantial tightening already pushed through catches up as we pass through the peak rate of rollovers. This is one of the factors behind the recent stabilisation in interest rates.

The buffers built into lenders’ serviceability assessments, which account for higher interest rates, will also help. The beginnings of the “fixed-rate cliff” originated under the tighter lending standards that have been achieved by various prudential measures in recent years.

Further, many borrowers have built savings buffers to handle rising interest rates – a process that has been well telegraphed.

Based on the loan book of Australia's largest home loan lender, the Commonwealth Bank, close to 4 out of 5 borrowers are ahead on their repayments with almost half of borrowers at least 6 months ahead. A third of those have a repayment buffer more than 2 years in advance. Though with the pressures on disposable incomes, these flows are lower than pre-pandemic averages and not necessarily representative of those with fixed-rate loans.

Another buffer comes as large value gains in the past few years mean many borrowers who refinance may be able to lower their loan to value ratio, offsetting the adjustment in servicing costs to a degree.

There’s no question that the mortgage cliff exists for a portion of borrowers and likely those at the lower end of the income distribution. For the small number of borrowers that find themselves without the above safety nets and with low savings buffers, lenders will cooperate to avoid mortgagee selling. Just as repayment holidays were offered through the pandemic period, there are dedicated hardship teams that will attempt to find a solution via potential loan restructuring options, such as longer loan terms, interest-only periods, or temporary repayment suspensions.

Provided the unemployment rate does not rise by a lot more than it is expected to do so, the cliff will be much less steep than many have speculated.

So far, the data available supports this conclusion and there are few signs of distress at present.

Listings coming to market have been subdued through the first half of this year providing little indication of a material uptick in motivated selling. That picture has begun to shift in Sydney and Melbourne in July but the uptick in listings volumes is largely attributed to prior weakness and improving confidence with interest rates having stabilised and prices continuing to rise.

According to the Australian Prudential Regulation Authority (APRA) non-performing loans and 30-day arrears remain very low compared to historical averages and well below pre-pandemic levels as up until the quarter ending 31 March 2023.

It would be reasonable to see some increase in arrears in the months ahead with mortgage servicing costs having increased so sharply. But so far, the predominant consequence in the housing market has been the refinancing boom.

It's inevitable that households with fixed-rate loans will experience a difficult period of adjustment and resilience will be tested as we pass through the eye of the storm. But there are many factors that suggest that the majority of households have some protection against future financial stress driven by the sharp move higher in interest rates.