The spring selling season has arrived, and there's good news for buyers who have faced limited options for much of this year.

Choice has improved significantly in the major capitals, with buyers benefiting from the rush of properties hitting the market.

Given the spring selling season has kicked off busily, and national home prices have grown for the eighth consecutive month — the longest stretch of growth since the pandemic period — many are now wondering how the selling season will shape up.

One driver of the recovery in home prices this year has been the subdued listings environment. The limited flow of new listings coming to market in the first half of 2023 meant buyers were competing over fewer properties, contributing to the lift in home prices so far in 2023.

Home prices have also been underpinned by record levels of net overseas migration, the challenged rental market and a shortage of homes.

In the face of such a substantial reduction in borrowing capacities and deterioration in affordability, the fast turnaround in home prices has been an unusual occurrence, and a testament to the strong demand from buyers.

However, the listings environment is now shifting, with the spring selling season blooming and activity on the rise.

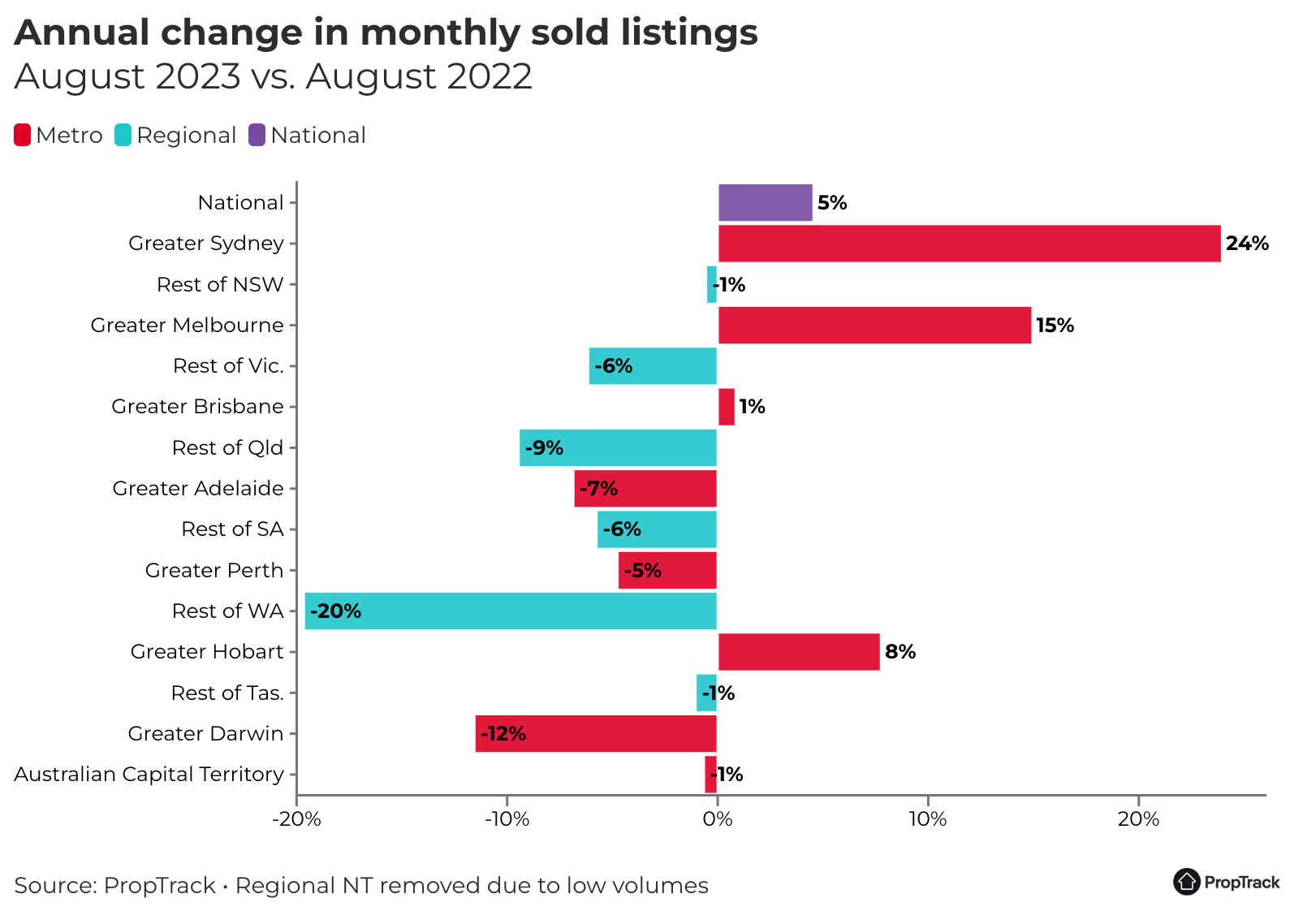

New listings volumes in August rebounded significantly in Sydney (+18.4% year-on-year) and Melbourne (+20.8% year-on-year), and both capitals recorded their busiest end to winter in more than a decade.

In other capitals there was a strong pick up in new listings compared to July as activity ramped up for the spring selling season. However, unlike Sydney and Melbourne, most still lagged the pace set in August last year.

Improved seller sentiment has been a key driver of the increase in listings, with confidence springing as interest rates remain on hold amid positive market conditions.

It’s become more and more likely that the peak in interest rates is here, and August was the third consecutive month the Reserve Bank has left interest rates on hold – welcome news for buyers and sellers alike.

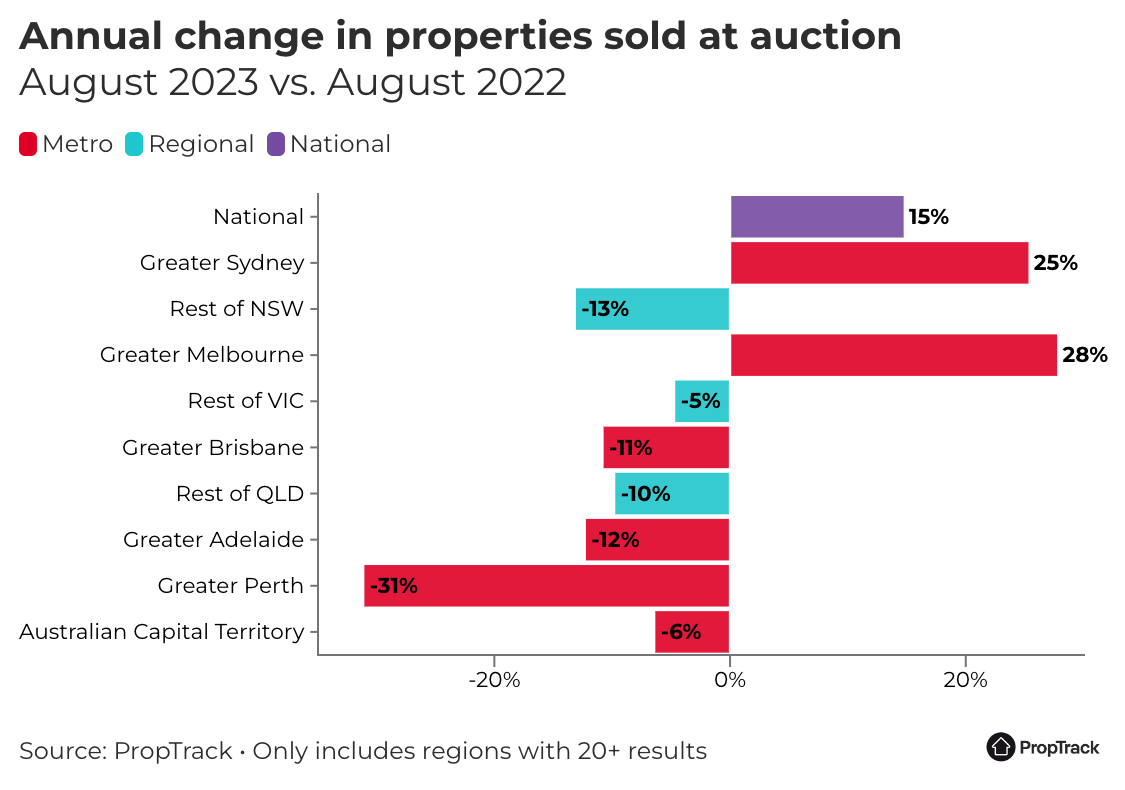

Auction volumes increased 15% in August compared to the same period last year at a national level, but were up 25% year-on-year in in Sydney and 28% in Melbourne.

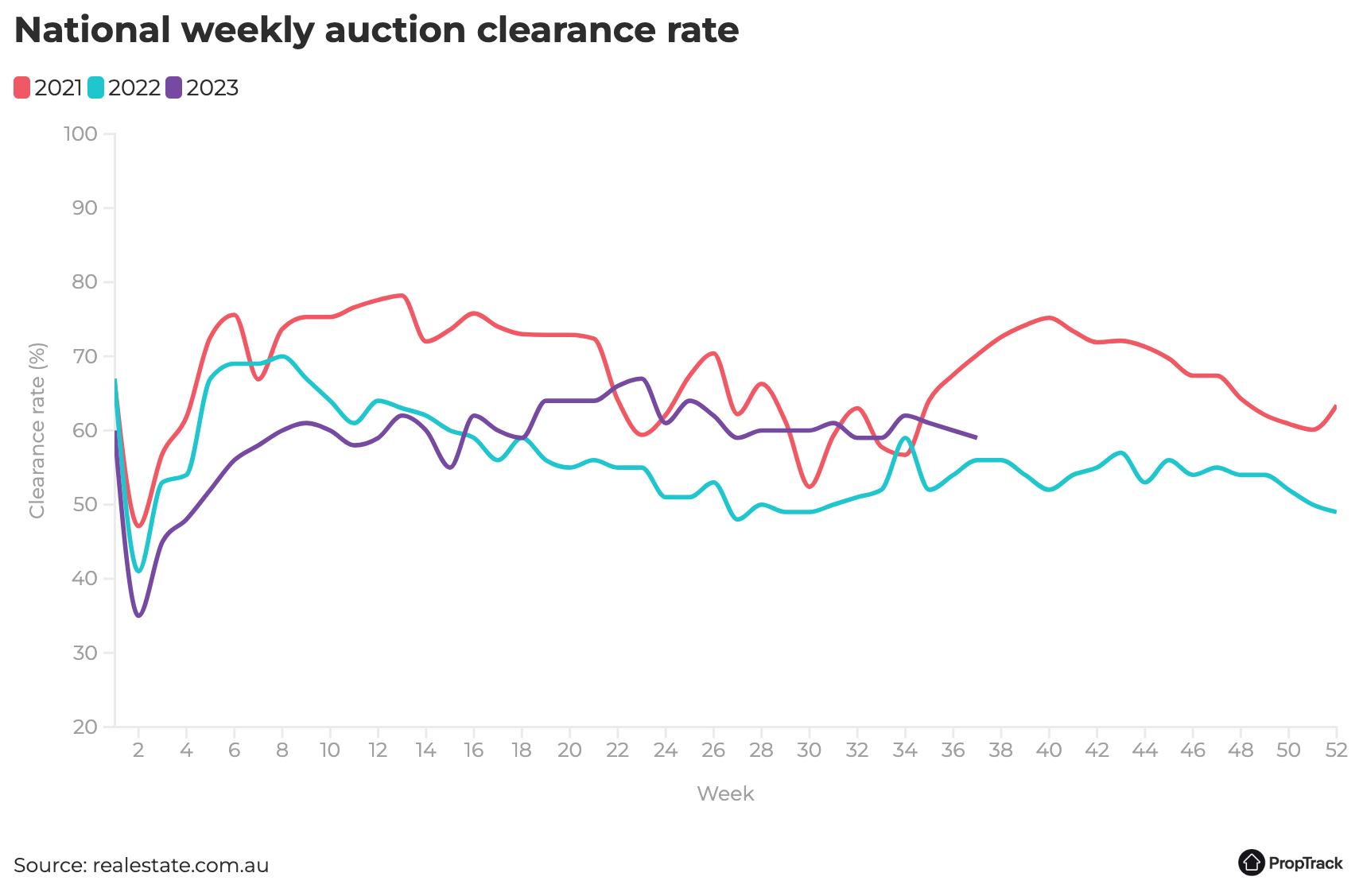

Whilst auction volumes have increased, clearance rates have eased in recent weeks, but remain above levels seen this time last year when interest rates were first rising.

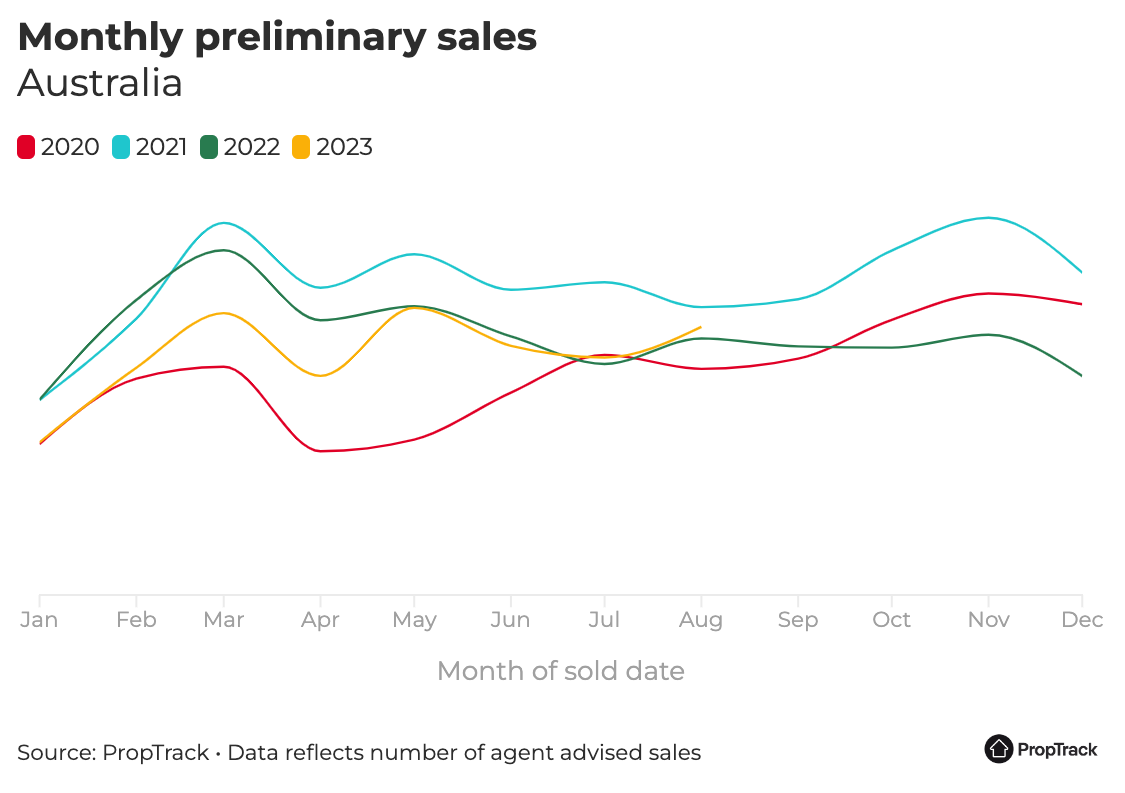

Sales volumes have also picked up, especially in Sydney where sales volumes increased 24% year-on-year in August 2023, with both buyer and seller confidence on the rise.

With this spring shaping up to be busier than last, supply and demand dynamics are likely to continue rebalancing in the coming months.

The uptick in the number of properties coming to market will challenge the extent of buyer demand as the selling season continues to unfold.

There is a possibility that home buying demand is able to absorb the uplift in new stock coming to market, given interest rates have peaked, the labour market remains tight, and population growth remains strong.

There are already signs this may be the case, and although there has been a pick-up in listing activity heading into spring, buyer enquiries on realestate.com.au have also increased.

The average number of enquiries per for sale listing held steady in August – an indicator that buyer demand is so far picking up inline with the uptick in properties coming to market.

However, with the flow of new listings having rebounded so significantly in Sydney and Melbourne, and likely to continue to do so, the pace at which prices have grown this year could still slow.

While prices are set to keep rising, the significant uplift in the volume of stock listed for sale gives buyers more choice and more bargaining power.

It’s a different story in the other capital cities.

Buyers in Hobart have enjoyed substantially more choice for much of this year, and with an uptick in activity in recent months, buyers in Canberra now have reasonably strong choice. The total number of properties available for sale in these cities is around the average seen over the past decade.

In Perth, total stock on market improved a little in August, but is close to record lows. As a result, buyers are continuing to compete for the fewer homes on the market.

In fact, market conditions in Perth have never been more competitive.

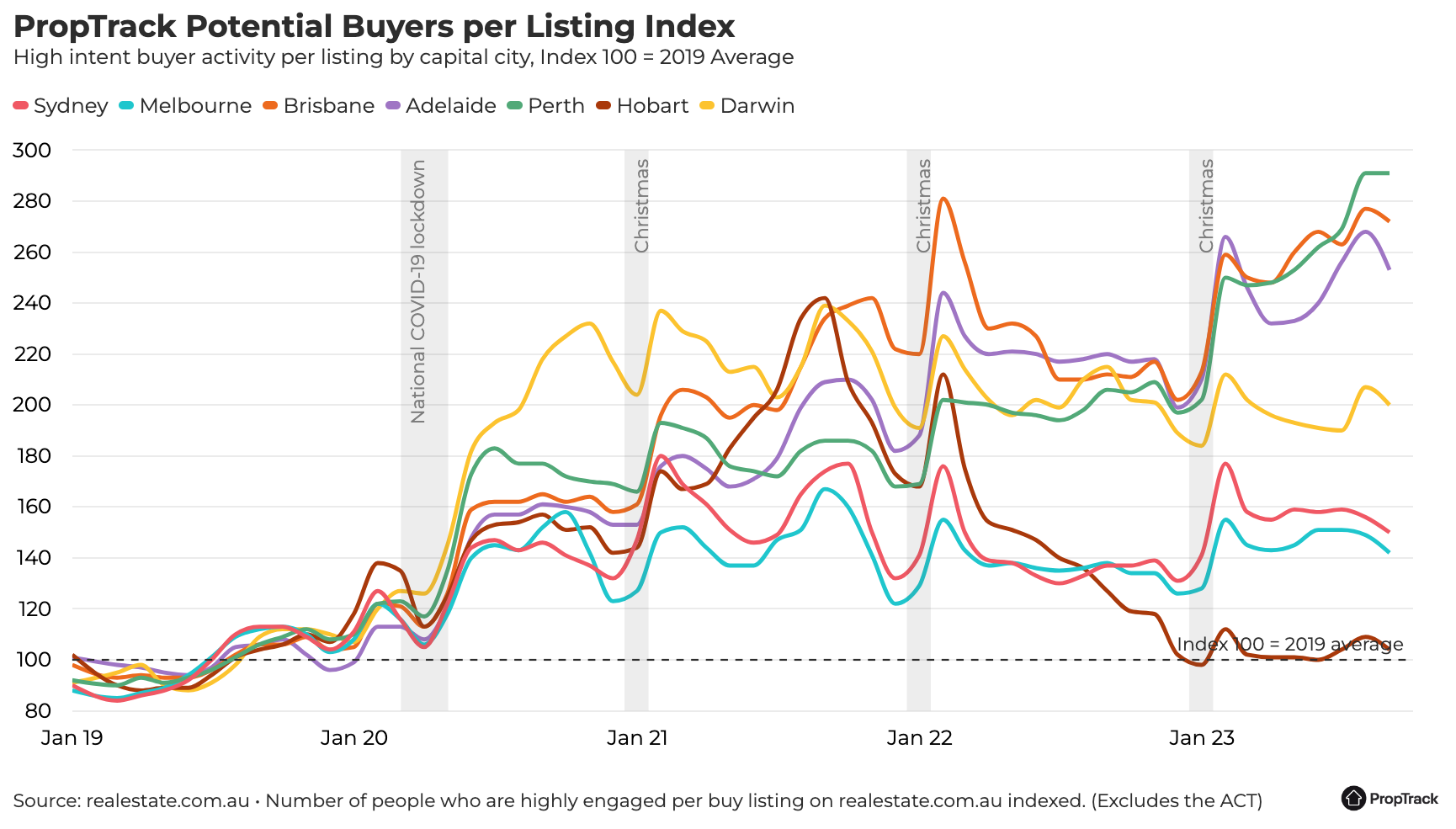

“Per listing” demand from potential buyers in Perth hit consecutive record highs in July and August after increasing 41.4% year-on-year in August 2023, making Perth the most competitive market in the country, according to the PropTrack potential buyer demand per listing metric.

The average number of enquiries per for sale listing in Perth also increased to a record high in August 2023.

This strong competition is likely one reason why Perth has overtaken Adelaide as the strongest performing capital city market over the past year, as buyers compete for limited options and affordability is less constrained.

Perth is closely followed by Brisbane and Adelaide, with conditions in both these markets remaining much more competitive for buyers.

Potential buyer demand per listing remains close to record highs and the total number of properties listed for sale, whilst improving in August, remains lower than a year ago and much lower than has been typical over the past decade.

In both capitals the average number of enquiries per for sale listing also increased in August, to hit the highest level since early 2022, before interest rates began to climb.

These factors point to potential divergent conditions throughout the spring selling season.

Price growth is likely to remain stronger in the smaller capital city markets of Perth, Adelaide and Brisbane, where choice remains limited and demand is bolstered by housing remaining comparatively affordable, as well as tight rental markets and both interstate and overseas migration.

In Sydney and Melbourne, conditions have shifted markedly, and the uptick in choice for buyers will likely bring more balance to supply and demand conditions as options for buyers improve. This could see the pace of price growth slow.

Meanwhile, Hobart and Canberra have seen more balanced conditions for many months and are already recording slower growth and recouping the price falls of 2022 at a much slower pace.

Further out, home prices are likely to continue rising while interest rates remain on hold at a level substantially higher than this time last year. As a result, affordability will continue to deteriorate, though not at the same pace as over the past 18 months, with price growth partially offset by growth in household incomes and wages.

The economy is forecast to slow, however international migration and population growth are forecast to remain strong, which will further add to housing demand. Coupled with lower new supply, a housing shortfall is likely to continue to underpin values as population growth increases, despite affordability remaining stretched.

Home prices in 2024 will also be influenced by whether interest rates begin to move lower. Many expect interest rates will be cut at some point in 2024, causing borrowing capacities to increase and mortgage servicing costs to decrease, likely fuelling a continued rise in prices.