The latest PropTrack Home Price Index showed the current price rebound continued in May, with price rises becoming more widespread across markets.

National home prices have now increased for five consecutive months, rising 0.33% in May, and are up 1.55% year-to-date.

The capital city markets are driving the recovery and prices are up 1.97% across the combined capitals year-to-date. In fact, home prices in the combined capital cities in May have recorded the strongest quarterly growth since the December quarter of 2021.

Looking at home price growth over the past quarter across smaller geographical areas it’s clear that price rises have become more widespread and, in many cases, the markets that led the price falls are leading the recovery.

This is most obvious in Sydney, the market that was first to see prices fall and that saw the steepest declines. Across greater Sydney all regions have seen a lift in prices so far this year.

The same is true in Brisbane where all regions have recorded a lift in prices so far this year.

In Melbourne all but two (Melbourne - North West and the Mornington Peninsula) of the metropolitan regions have recorded a quarterly increase in home prices.

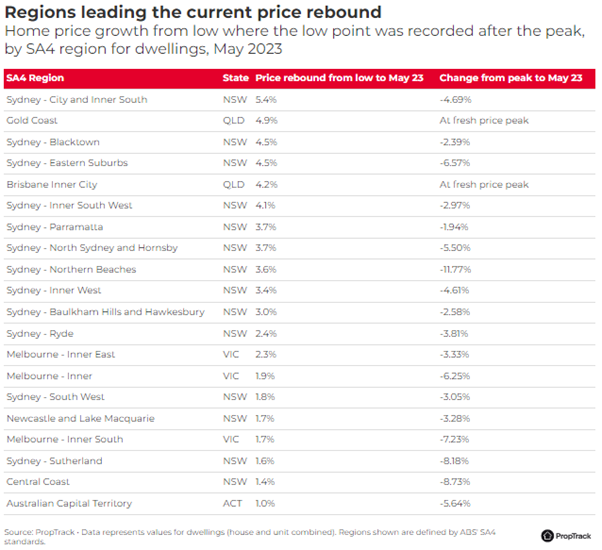

Looking at the regions where home prices fell, but are now rebounding quickly, also gives an understanding of which markets are leading the recovery and where stronger housing demand is in play.

This is done by analysing home price growth across regions that have experienced the strongest price growth since their last low, where the low point was recorded after the peak.

Home prices in some markets have already completely erased their falls and surpassed their prior peak.

In the Gold Coast, price falls have reversed entirely. Home prices there peaked in April 2022, fell 3.1% to their low in September 2022 and have now risen 4.9% to reach a fresh price peak. In Brisbane Inner City, prices also peaked in April 2022, fell 3.6% to their low in December 2022 and have now risen 4.2% to reach a new price peak.

The year began with stronger housing demand bolstered by the rebound in net overseas migration, and tight rental markets. Combined with a scarcity of listings buyer interest has been concentrated, which has underpinned home prices.

These dynamics have continued into the fifth month of the year, with stronger housing demand relative to supply on market continuing to see home prices lift, offsetting the downward pressure from continued interest rate rises.

Although supply constraints eased slightly with respect to the total stock on market in some regions, the flow of new listings remains soft, keeping a floor under prices with sellers benefitting from lower competition with other vendors.

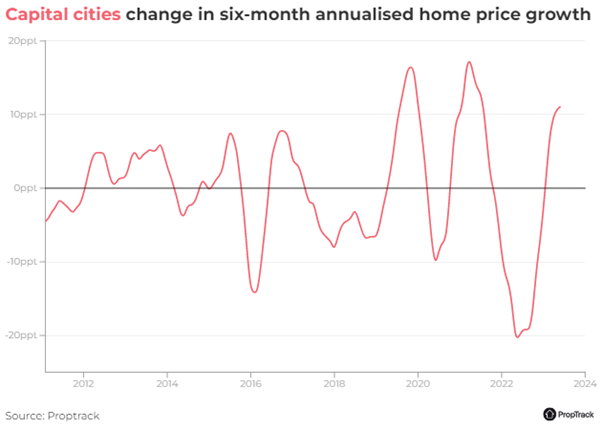

Sydney has seen a rapid turnaround in home price growth. Annualised three-month price growth in Sydney, the market leading the rebound, is sitting at 8.1%, 12.1 percentage points higher than the negative annualised three-month growth of six months ago in November of 2022.

Canberra and Brisbane have also recorded a rapid turnaround in prices, with their annualised three-month price currently sitting at 4.1% and 5.8%, respectively.

Adelaide is a market where recent price momentum has been strong, having bucked the price falls seen in most markets in 2022. The annualised three-month change in Adelaide home prices is 7.8%.

The improvement in market conditions is becoming more pervasive, with the pace of price growth in Adelaide accelerating as conditions have strengthened.

The decision by the Reserve Bank to lift the cash rate in May did not deter the current home price rebound, in fact the opposite occurred, with price rises broadening across markets and remaining resilient to the falls the calculated shift in borrowing capacities would imply.

Housing demand is stronger, likely bolstered by the surge in net overseas migration, as well as very tight rental markets. Given limited new stock is coming to market, buyer interest is being concentrated, which is underpinning home prices and offsetting the downward pressure from interest rate rises.

Further, the unemployment rate is close to a multi-decade low, promoting a sense of job security. Wages growth, while running behind inflation, has also increased.

Five months of price rises that have gathered traction across markets could also be drawing buyers off the sidelines. Many buyers and sellers anchor expectations from recent momentum, which can then embed trends in market.

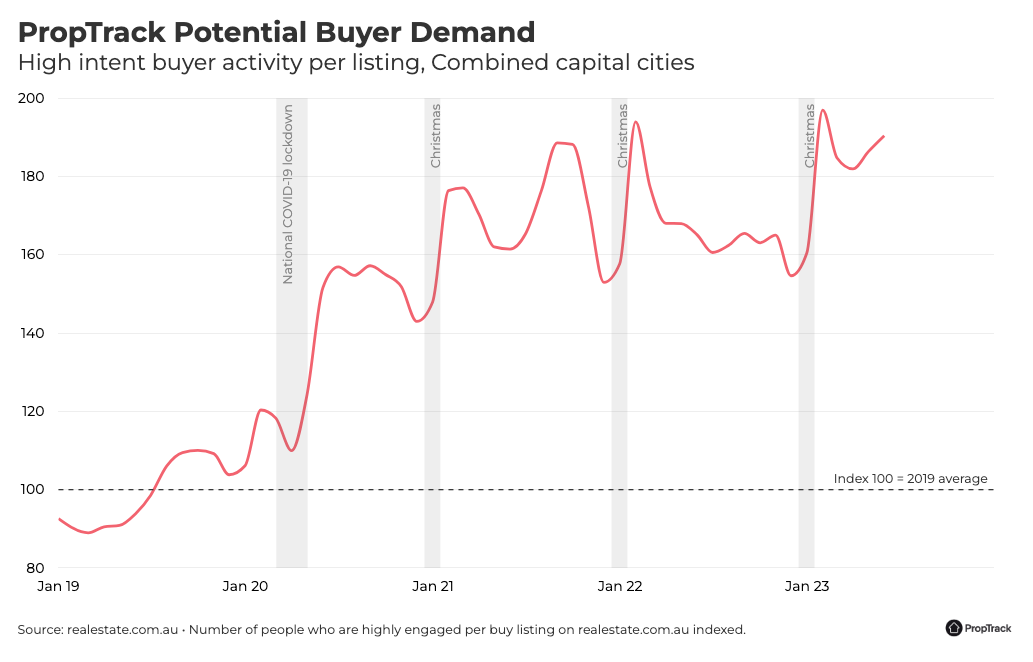

Demand from potential buyers as measured by the number of potential buyers per listing has increased 3.1% over the past quarter across the combined capital cities. Demand to buy in the capital cities is 15% higher than in May 2022, and more than 20% higher than levels seen at the onset of the spring selling season in 2022, when interest rates were quickly rising and prices were falling in most markets.

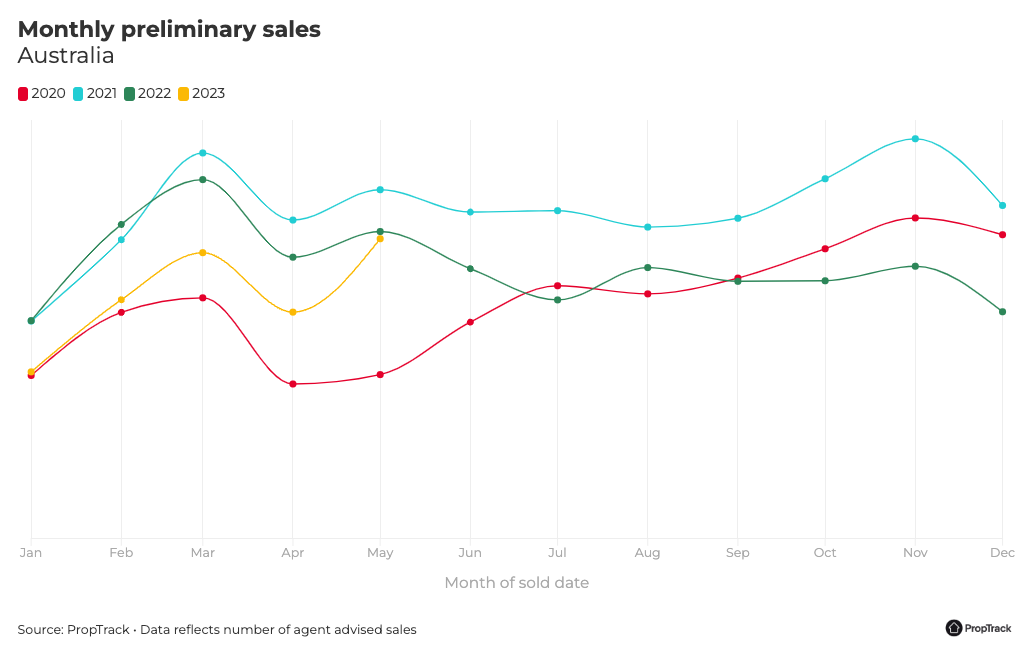

As the recovery has broadened numerous metrics are reflecting the improvement in conditions; sales volumes have increased and auction clearance rates have also improved and are now holding firm above levels seen in the back half of 2022.

Across the capital cities in May 2023 preliminary monthly sales increased 32% month-on-month and were 1.9% higher than levels seen in May 2022. This has been led by a strong increase in Sydney where preliminary monthly sales were 15.2% higher than levels seen in May 2022.

Though national home prices have now moved through their fifth month of growth, a bottoming process is seldom linear and the outlook for prices remains uncertain.

The RBA has reaffirmed its commitment to overcoming the challenge of high inflation and anchoring inflation expectations. Interest rates rose again in June and look set to increase further. The economy is also expected to slow, which is likely to slow the home price recovery, particularly with the seasonally slower winter market approaching.

The unemployment rate is expected to continue to lift in the coming months, this could mean buyers become more cautious once again as their sense of job security wanes.

The months ahead will see an increase in the number of borrowers who took advantage of record low fixed rate mortgages throughout the COVID period rolling onto mortgage rates that are substantially higher.

This increase will be countered to a degree by large savings made throughout the cheap fixed period. And for those who are able to refinance with a different lender, the level of competition – with less buoyant credit conditions seeing some lenders offering discounts – will also provide some respite.

In addition to liquidity buffers, strong home price growth throughout the pandemic means many households have substantial equity buffers in their homes. Current labour market conditions also provide a safety net for many households.

However, there is no doubt that this will be a challenging period, with substantial budgetary adjustments required in the face of cost-of-living pressures biting elsewhere. Though, for the most part, homeowners are likely to prioritise their mortgage repayments, preventing a significant uplift in distressed sales.

The current pace of price growth would also wane if stronger market conditions improve seller confidence and spark a boost in stock coming to market in spring.

Though, by that point interest rates could have stabilised easing buyer concerns. Interest rates are already closer to their peak than not, and the shock of rate rises has lessened. With the bulk of interest rate tightening in the rear-view mirror, much of the uncertainty buyers have experienced with respect to borrowing capacities and mortgage servicing costs is subsiding, meaning a better sense of how far their budgets may go.

While the pace of price rises is likely to slow as interest rates climb further and/or if the listings environment changes, some of the factors precipitating stronger housing demand will persist.

Population growth, tight rental market conditions and an undersupply of new homes are expected to remain.

As a result, most capital city markets will likely return to positive annual price growth in the coming months if stronger demand holds up against the expected slowing of the economy and growth continues.