The strength and pace of Australia’s market rebound despite surging interest rates surprised many this year.

At the start of 2023, we forecast that national home prices would fall. In November 2023, home prices had increased by 5.5% year-to-date.

This is despite increases in interest rates over the year, which led to housing affordability sitting at its lowest level in decades.

Key trends shifted compared to 2022 and contributed to the stronger than anticipated price growth.

At the end of 2022, sales volumes were sitting at similar levels to those in late 2019, having persistently declined as official interest rates were lifted every month from May 2022 onwards. In early 2023, there was a strong rebound in sales volumes that continued throughout the year.

Along with sales volumes, buyer activity increased significantly this year, with the number of enquiries per listing on realestate.com.au higher than a year ago throughout most of 2023.

Download the PropTrack Property Market Outlook December 2023 report.

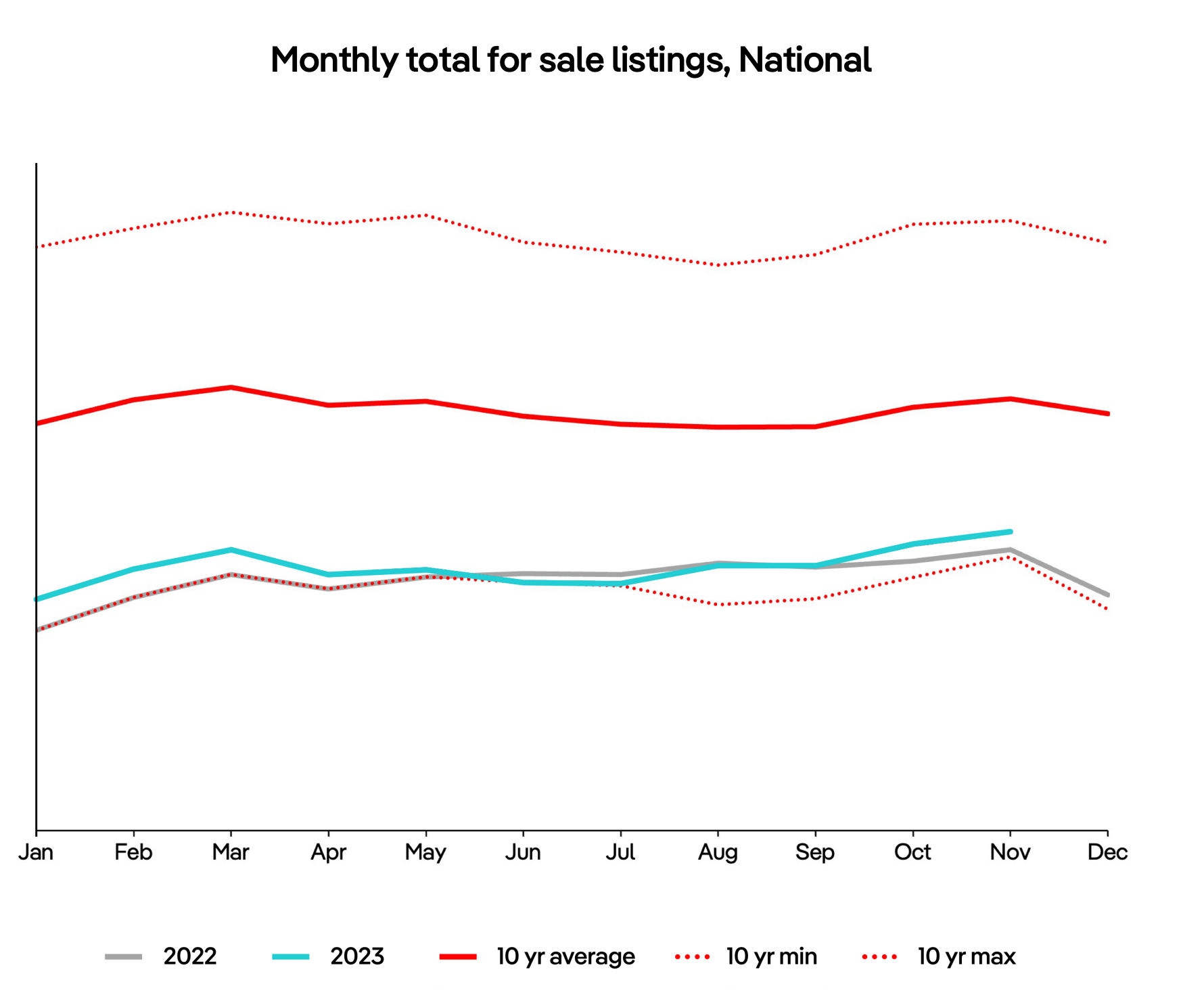

The total number of properties available for sale remained at persistently low levels in 2023. Buyers had little choice, which created significant competition. New listing volumes on realestate.com.au did increase from the middle of the year, mostly in Sydney and Melbourne.

However, the lift in supply did little to moderate price growth other than slow its pace, which is a common trend we’d otherwise see in spring when more properties come to market.

The escalation in the cost of new home builds, due to increasing material prices and labour costs, saw demand for new housing decline. This helped to support demand for established housing, but the lack of new supply is clearly problematic for the market over the long-term.

The low volume of supply for sale in certain markets, coupled with established home price rises, is likely to see buyers seek out new homes because they are unable to find and secure properties in the established market.

Another major factor supporting prices in 2023 was the significant demand for housing, which was fuelled by rapid population growth. Over the 12 months to March 2023, the population of Australia increased by 563,205 persons. For perspective, that is just shy of the population of Tasmania being added to the country in one year.

More up-to-date indicators from overseas arrivals and departures data show little evidence of a slowdown. The impact of rapid population growth has largely been felt in major capital city rental markets but is also contributing more broadly to strong overall demand for housing.

From January to November 2023, property prices increased by 5.5%. Capital city prices were 6.6% higher and regional prices were 2.8% higher.

Over the year, house prices have risen at a moderately faster pace than unit prices, with increases of 5.6% and 5%, respectively. It should be noted that capital city house prices are rising faster (6.9%)

than units (5.3%).

The trend is reversed in regional markets, with stronger unit price growth (4.2%) than houses (2.5%).

While prices have continued to rise, the rate of price growth has slowed over recent months. This slowing has coincided with a lift in new listings on realestate.com.au. However, the slowing has also

been apparent in areas that haven’t had a significant increase in new listings. There is a lagged impact of interest rate rises and many borrowers have shifted from fixed rates to variable rates throughout

this year, which may also be impacting on price growth.

Sales volumes in 2023 have been much stronger than those recorded in late 2022. Preliminary sales volumes on realestate.com.au in November 2023 were 15.9% higher than November 2022. Even though there has been a moderate increase in listings coming to market, we have seen a pick-up in sales, despite much higher interest rates.

The number of new listings coming to market was higher than it was a year ago, up 4.7% in November.

Despite the increase, new listings were still 2.8% lower than the November 10-year average. The lift in new listings is largely being driven by Sydney and Melbourne, with new listings remaining well below their long-term average in other major capital cities.

Although there has been a lift in new listings, total listings remain historically low, affording buyers relatively little choice as they begin their property search.

Total listings are up from a year ago but are 23.9% below their November decade average. Again, there is a discrepancy between Sydney and Melbourne compared to other major capital cities. Total listings in Sydney and Melbourne were 1.6% and 10.8% higher than their November decade average.

In Brisbane, Adelaide, and Perth, total listings were more than 30% below their November decade average.

The number of enquiries per listing on realestate.com.au has been trending higher throughout the year and was 20.5% higher than at the same time last year in November.

In each of the major capital cities, the number of enquiries per listing was higher than a year ago, despite the overall number of listings in most cities also being higher than a year ago. This highlights the strong interest in housing.

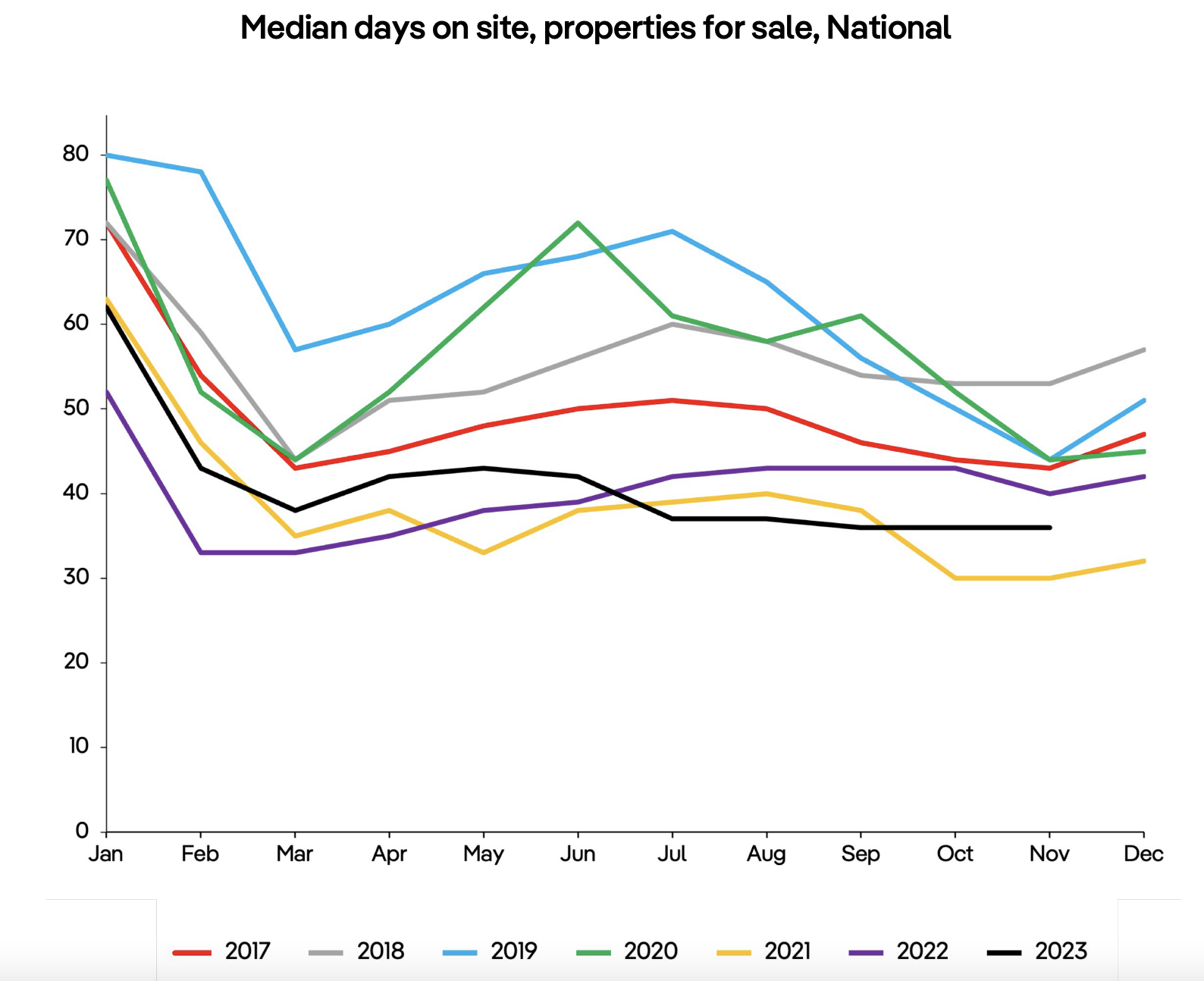

The median number of days properties are advertised on realestate.com.au has fallen from 40 days a year ago to 36 days, despite the annual increase in stock for sale. This also highlights strong demand for properties. In each of the major capital cities, days on site is now lower than it was a year ago.

Looking at home prices in 2024, it’s important to consider the current market trajectory, where interest rates could head, what could happen with housing supply, and the impact of the interest rate hikes that have already occurred.

Last year’s forecasts were based on an assessment that interest rates had increased rapidly and that the subsequent reduction in borrowing capacities and deterioration in housing affordability would lead to fewer sales and more stock for sale, driving prices lower.

It makes sense that a reduction in borrowing capacity would result in lower prices but that has not come to fruition. The market proved resilient, with few forced sales, and price growth and demand lifting in 2023.

After interest rates had been on hold for several months, September quarter inflation data was outside of the RBA’s tolerance. As a result, it lifted official interest rates by a further 25 basis points in November 2023, taking the cash rate to 4.35% – the highest it has been in 12 years.

Despite higher interest rates reducing borrowing capacities and housing affordability, a large depreciation in prices over 2024 is still unlikely.

From the middle of 2024, we’ll also see the commencement of stage three tax cuts, which are most beneficial for higher income earners. In-turn, this could lead to increased demand for higher priced housing.

We expect that price growth will be slower in 2024 than in 2023. In saying that, we are anticipating persistent strong demand for housing, limited new housing construction, and an expectation that total listing volumes will remain low with uncertainty around whether new listing volumes will be as strong as they have been over the second-half of 2023.

These factors will likely lead to further price gains.

Angus Moore, PropTrack senior economist

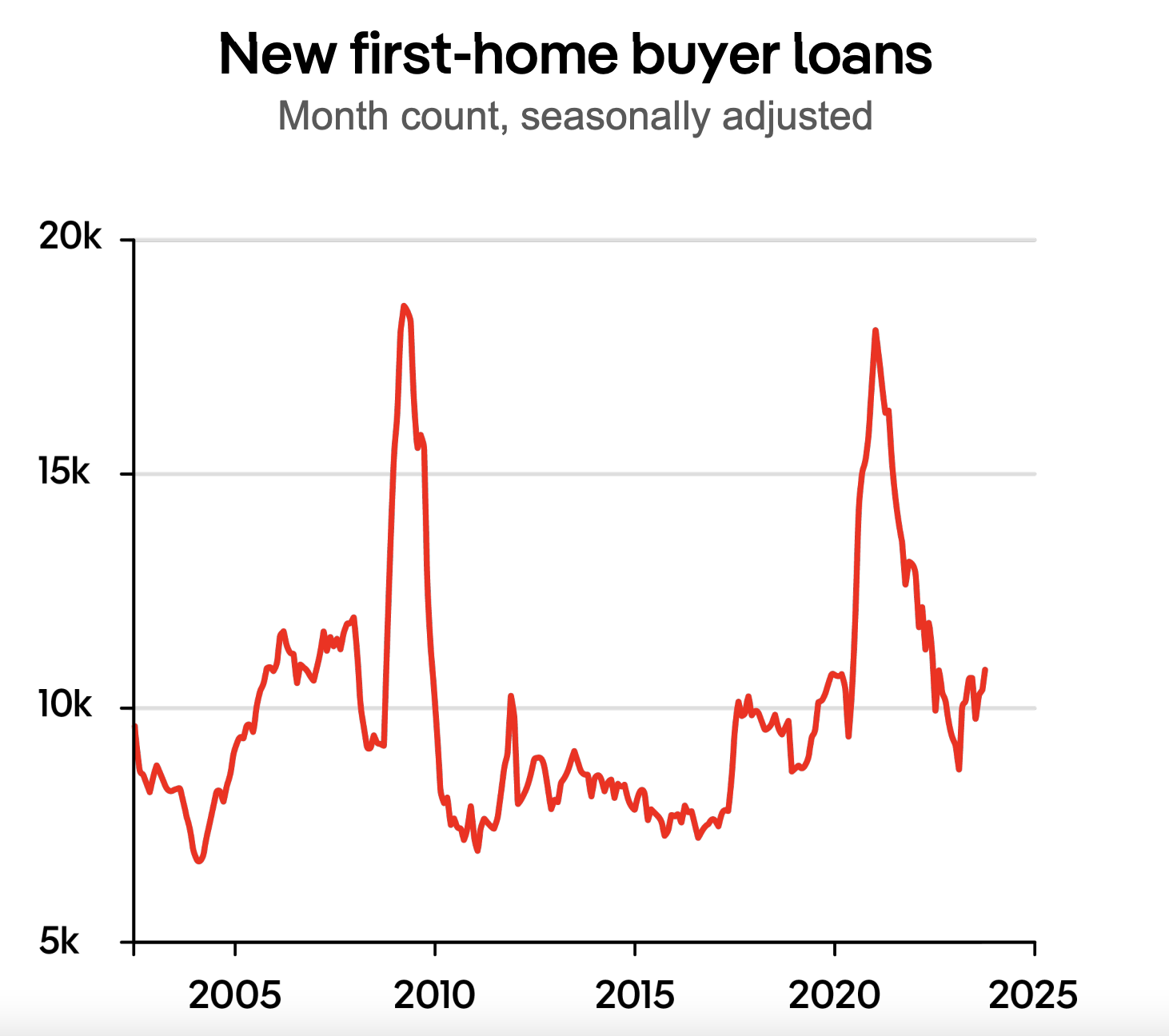

Pandemic-era low interest rates saw a wave of firsthome buyers entering the market. In 2021, more than 160,000 first-time buyers took out a mortgage – close to twice the number of first-home buyers than was typical in the decade prior to the pandemic.

Rapidly rising interest rates throughout 2022 and in to 2023 have chilled first-home buyer activity.

In 2022, there were about 30% fewer first-home buyers. While housing markets have stabilised in 2023, first-home buyers have stayed quiet. To date in 2023, activity has been even more subdued than in 2022.

A key driver of the decline in both first-home buyer activity and home prices in 2022 was significantly

worsened housing affordability.

The PropTrack Housing Affordability Index shows that, by mid 2023, housing affordability had hit its worst level in at least three decades.

Unless the outlook changes materially, this situation is unlikely to improve much, meaning first-home buyer activity is likely to remain subdued.

Home prices are expected to increase, albeit modestly, which will further strain affordability. While the outlook for interest rates is a key uncertainty for 2024, the RBA’s recent forecast for inflation implies little chance that interest rates will decline, and it is possible they will increase further.

Balancing these factors, wages are growing at their fastest rate in more than a decade, aided by an extremely tight labour market. Higher incomes will help offset higher mortgage costs, but it will be a slow

process.

The fact that affordability is likely to remain very stretched, and demand from first-time buyers remain subdued, is part of why we expect home prices nationally will grow at below-average pace over 2024.

Anne Flaherty, PropTrack economist

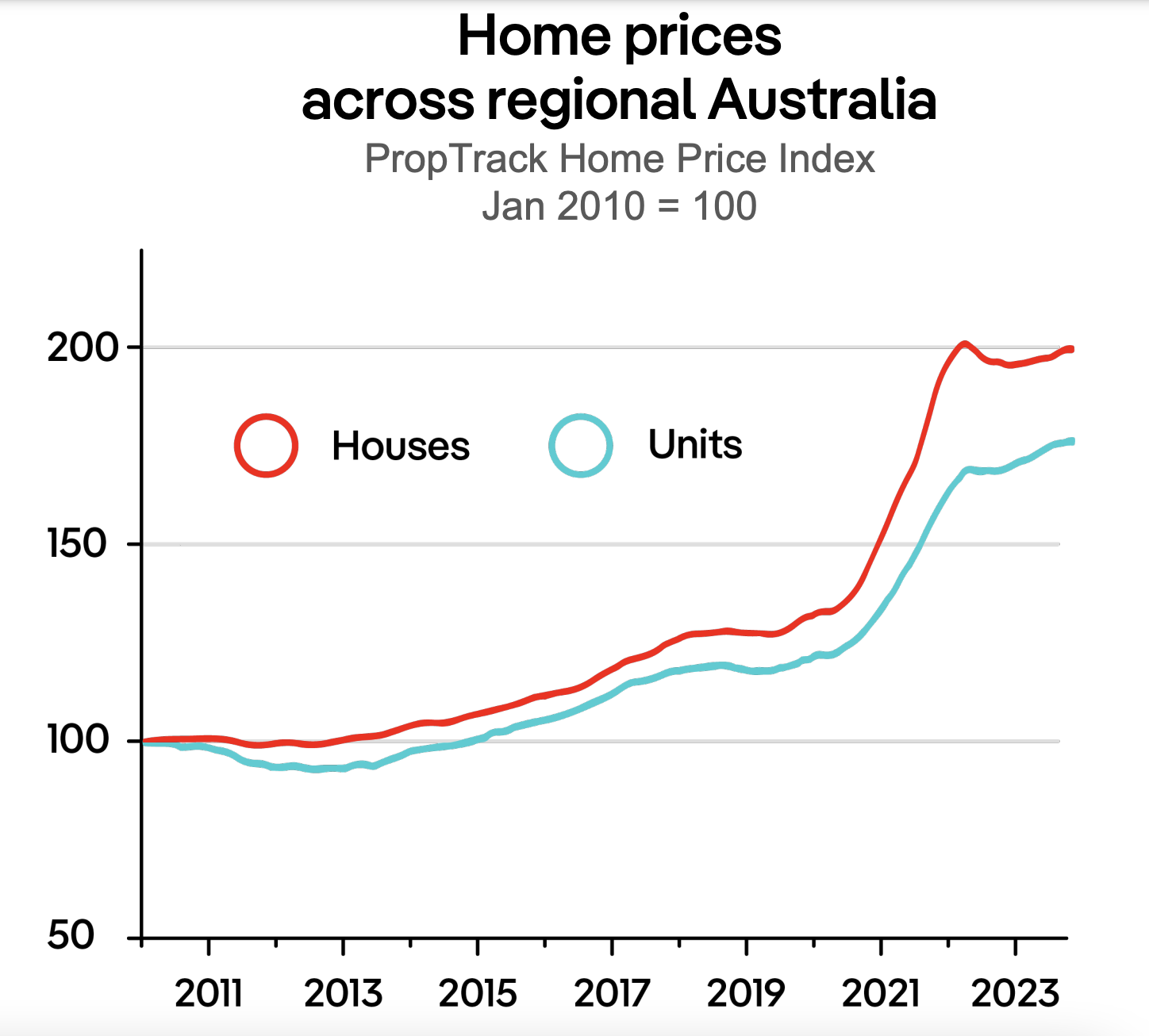

Australia’s pandemic lockdowns led to a surge in demand to buy and rent regionally, driving an outperformance in price and rent growth in regional areas compared to capital cities. As of November 2023, regional home prices were sitting 49.8% above the levels seen in March 2020, well above the 32% growth recorded across the combined capital cities.

This trend has now reversed, and regional home prices have risen at less than half the speed of capital cities over the past 12 months (2.6% versus 6.5%). While regional home prices have increased every month so far in 2023, growth is subdued relative to the levels seen during the pandemic years.

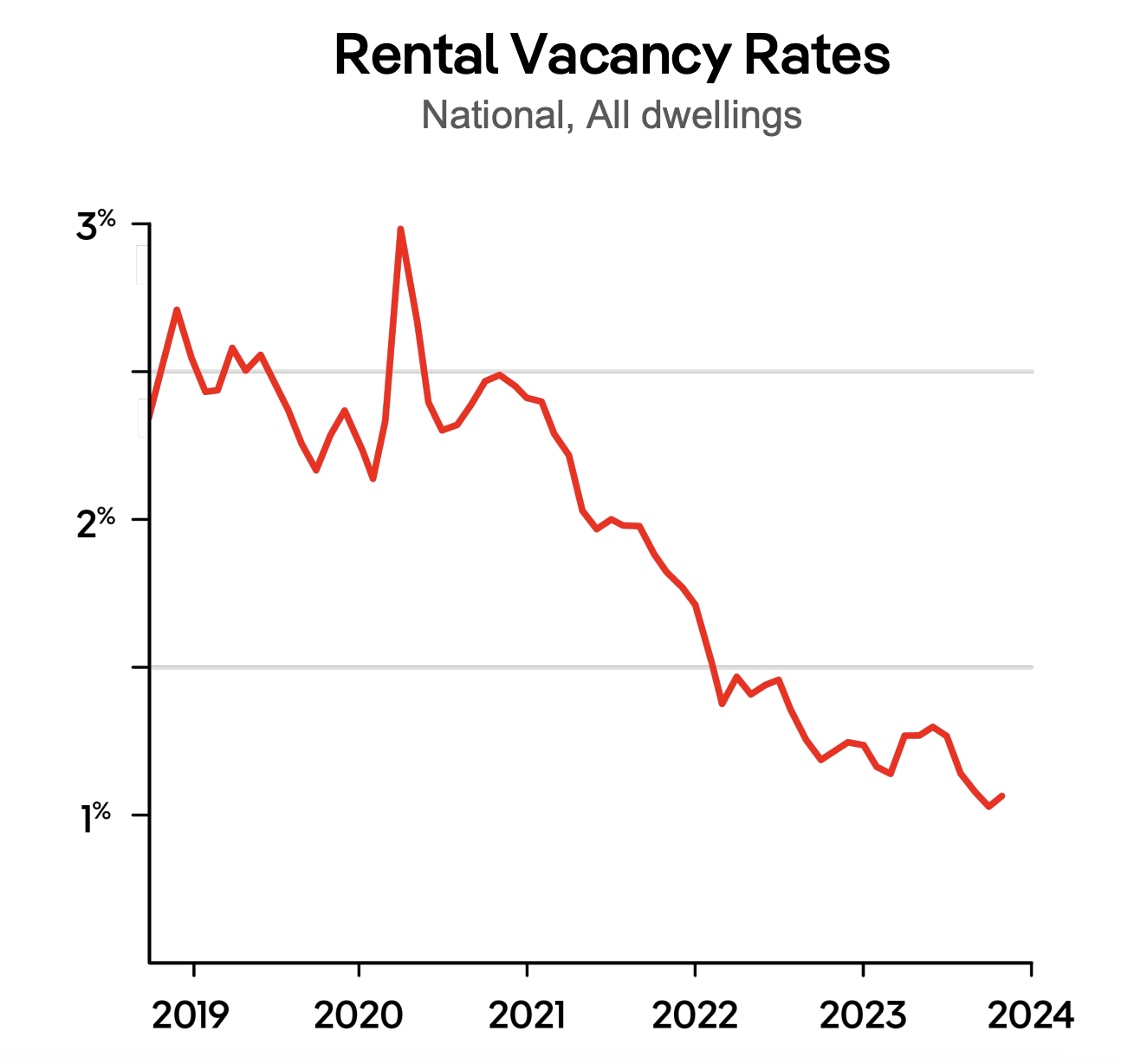

Regionally, demand for rental properties surged during the pandemic, with the vacancy rate hitting its lowest point at just 0.8 per cent in late 2021.

Following the end of lockdowns, demand for rental properties cooled and the vacancy rate steadily rose over 2022.

The situation is now deteriorating again in the regions, with vacancy falling over the past six months, reaching 0.98% in November, below the level seen in capital cities.

While the pandemic drove an outperformance, positive net intrastate migration away from capital cities into regional areas has been a trend for over 20 years. With affordability currently at record low levels, more home buyers will be pushed further out to the regions and this trend is expected to remain.

Price growth is forecast to continue into 2024, with the supply of homes for sale predicted to remain subdued relative to buyer demand. Furthermore, population growth is likely to outpace development activity, which will continue to be hampered by high costs and build times. Similarly, rents are expected to continue rising across regional markets off the back of low levels of vacancy.

Paul Ryan, PropTrack senior economist

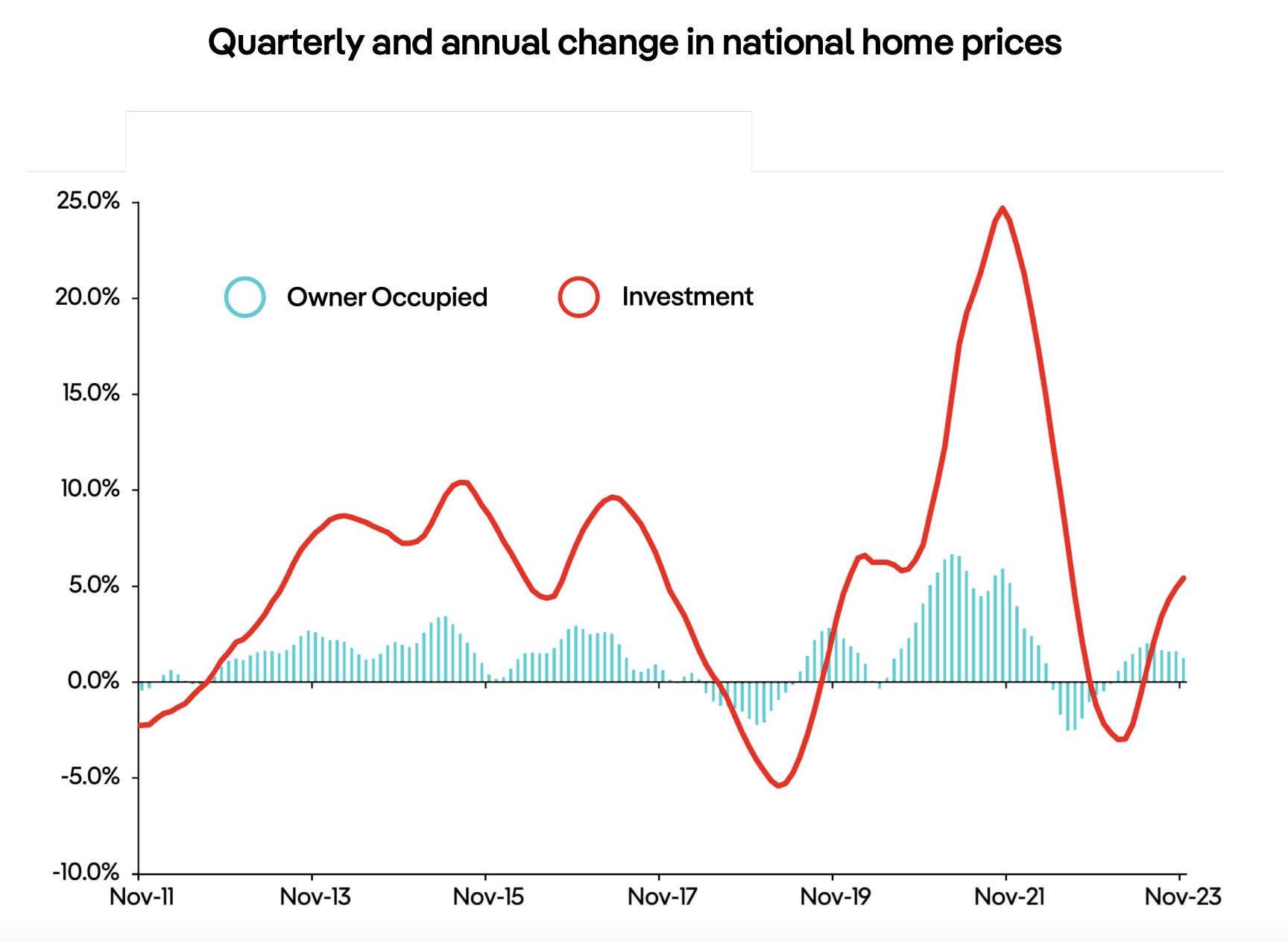

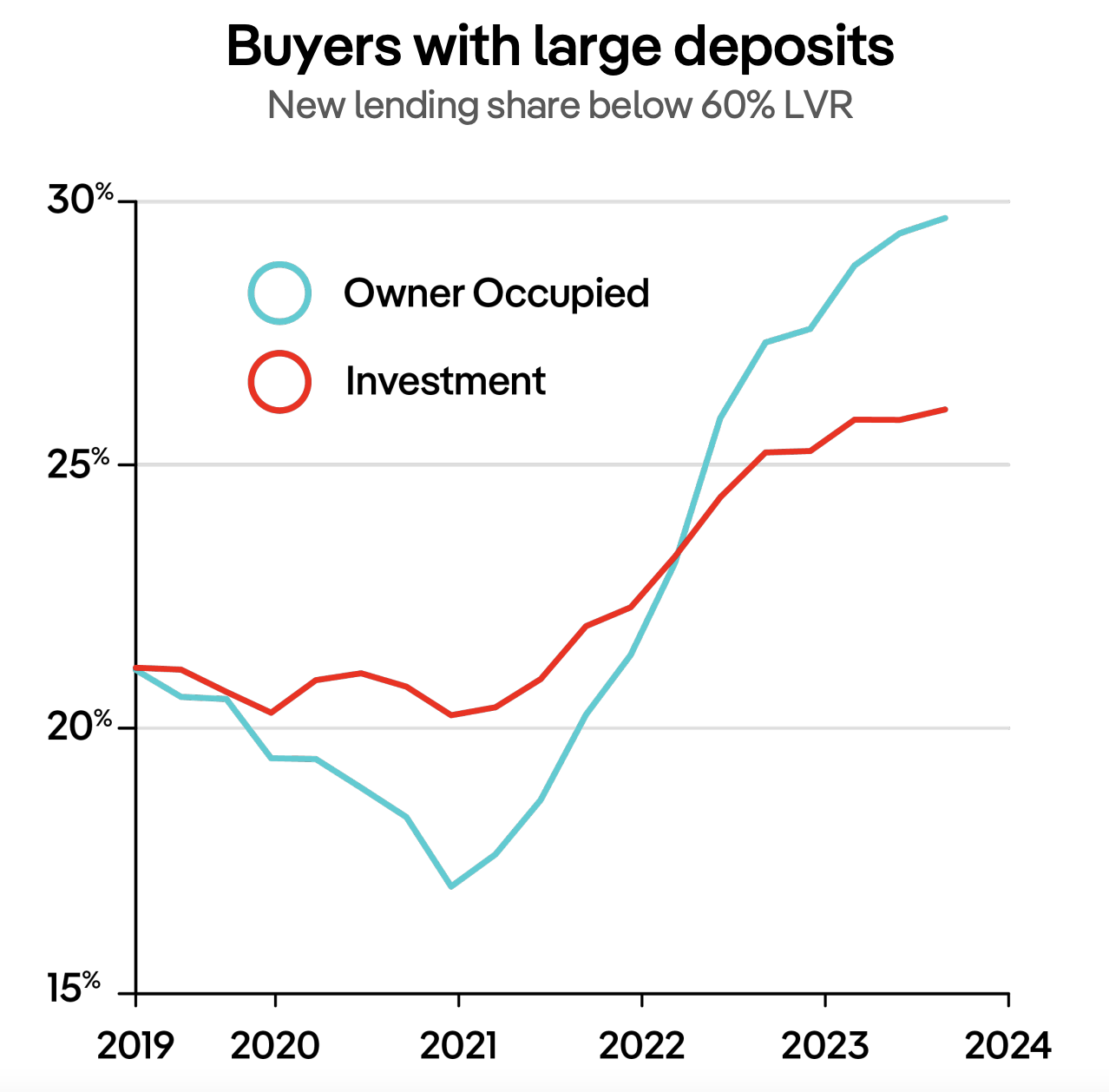

A key influence on home prices in 2024 will be the activity of upgrade buyers. A higher share of borrowers with large deposits is one reason why prices in 2023 have been so resilient to higher

interest rates.

Over 2023, an increasing share of lending was to those bringing large deposits to the purchase.

This was most evident for owner-occupiers. In the most recent data, almost a third of new lending was to owner-occupiers borrowing less than 60% of the value of their home. This share has almost doubled from levels seen in the middle of the pandemic.

Investor high-deposit lending has also seen an increase to more than a quarter of new lending. While this partly reflects higher refinancing activity, many in the market in 2023 were upgrade buyers taking advantage of large equity boosts from the pandemic boom, which saw prices increase 36% since early 2020.

High-deposit buyers are more insulated from the higher interest rate environment, but the question for 2024 is: how many of these upgraders are left?

Buyers with large deposits will likely continue to make up a higher share of the market in 2024, and play a part in keeping prices elevated, despite higher interest rates.

Eleanor Creagh, PropTrack senior economist

Australia’s rental market remained incredibly challenged in 2023, and provided one of the opposing forces countering continued interest rate rises and contributing to the strong pace of home price growth seen this year.

Extreme tightness in the rental market illuminates Australia’s housing shortage. With vacancy rates historically low, weekly rents are growing at a fast pace. There is nothing meaningful on the horizon to suggest a sufficient increase in supply of available rentals, which is the release valve we need.

With continued strong demand to rent, tight rental markets and upward pressure on rental prices are likely to remain in 2024.

The good news is that conditions are unlikely to deteriorate at the same pace as they have in 2023.

Challenging rental market conditions have likely incentivised those with the means to purchase sooner than they otherwise would have. Tight rental markets and strong rental price growth also entice investor activity, as well as perpetuating a shortage of stock for sale, a factor that underpinned prices this year.

As such, tight rental markets and strong rental price growth are likely to continue to buffer home price

falls. Though, this positive tailwind is expected to work with easing influence, providing one reason as to why the strong pace of home price growth seen in 2023 is expected to slow in 2024.