For homebuyers, and first-home buyers in particular, the question of whether to buy or rent a home is complex, with many costs and benefits to consider, both financial and emotional.

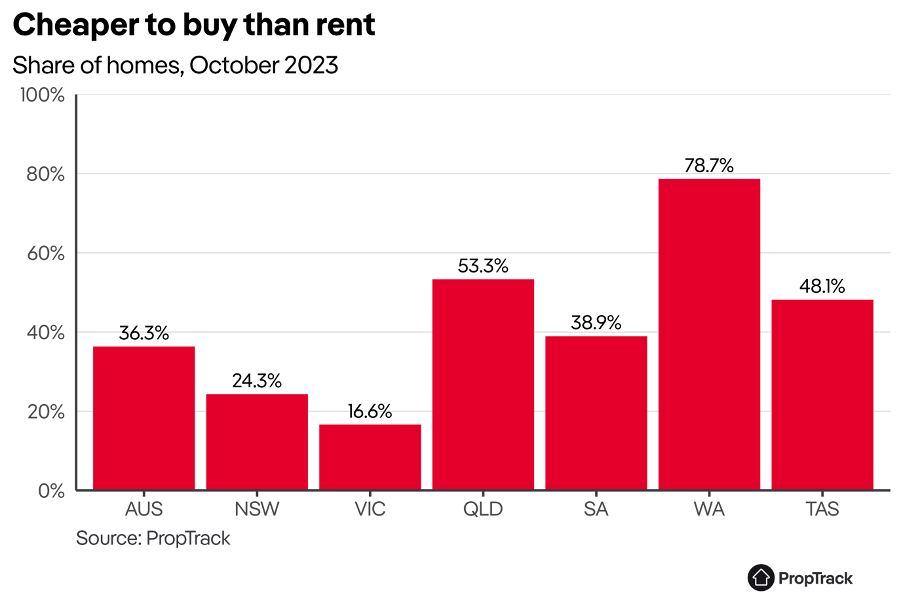

Comprehensive analysis by PropTrack into the financial costs and returns shows that more than a third of homes across the country are cheaper to buy than rent.

This is despite sharply higher interest rates which have pushed up the cost of owning.

Average new mortgage rates for owner-occupiers are now more than 6% following the sharpest pace of interest rate increases on record. But rents are also increasing strongly, with advertised rents growing 14.6% over the past year.

Across the country, differences in home prices and rents mean the financial attractiveness of buying a home can vary considerably.

In New South Wales and Victoria, less than a quarter of homes are calculated to be cheaper to buy than rent. In these markets – where prices tend to be higher than elsewhere – renting may make more sense for many.

But for others, there continue to be good buying opportunities.

And elsewhere across the country buying conditions are much more favourable.

In Western Australia, over three quarters of homes are calculated to be cheaper to buy than rent.

In Queensland more than half of homes are estimated to be cheaper to buy, despite prices increasing by more than 50% since the pandemic.

It is no surprise that one of the key reasons people continue to move away from NSW and Victoria is to take advantage of more favourable housing affordability.

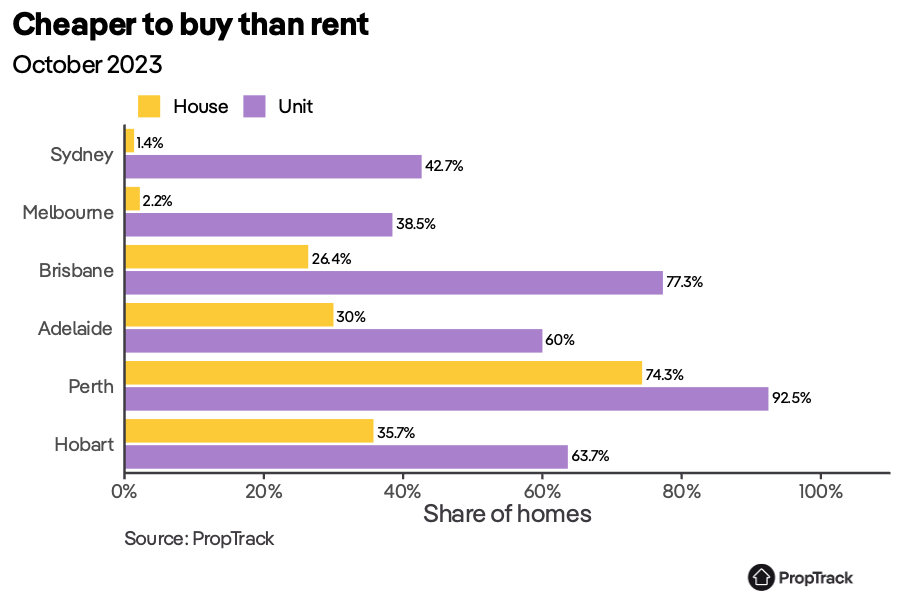

Units tend to be more favourable to buy than rent. Across the country more than half of units (55%) are cheaper to buy than rents, compared with just 29% of houses.

In Sydney and Melbourne, very few houses are estimated to be cheaper to buy than rent based on current purchase and rent costs, with as few as 1.4% of houses in Sydney being cheaper to buy.

But even in these expensive markets, there are opportunities for purchasers if they look at units – with around 40% of units in Sydney and Melbourne cheaper to buy.

Buyers looking for houses will find much more favourable conditions in Brisbane, Adelaide, Perth and Hobart – with Perth seeing almost three quarters of houses cheaper to buy at current prices. In Perth almost all units are estimated to be cheaper to buy.

This analysis presents a comprehensive comparison of the expected total financial costs of buying and renting.

The analysis uses PropTrack’s automated lender-grade estimates of the current price of buying and renting homes across Australia and estimates the total cost of owning and renting each home over the next 10 years.

| Inputs | Assumptions |

| Tenure period | 10 years |

| Mortgage rate | 5.98% per annum |

| Loan type | 20% deposit, 30 year term |

| Housing price growth | 3% per annum |

| Selling costs | 2% of home value |

| Rent growth | 3% per annum |

| Rental bond | 4 weeks rent |

| Maintenance or strata costs | 1.5% of home value per annum |

| Stamp duty | From state schedules |

| Investment return | 7% per annum |

| Inflation | 2.5% per annum |

Key to these estimates are mortgage costs, as well as other costs of owning and renting, including stamp duty, rates and maintenance.

In addition, the financial outcome depends on how future prices and rents evolve, as well as the alternative use of upfront buying costs, which we assume to be invested.

If prices and costs evolve differently, this will impact our projections of the financial favourability of different ownership options.

The results of this analysis show that buying conditions remain relatively favourable in Western Australia and Queensland, despite strong recent price growth.

This points to continued strong housing market performance in these regions, as many who are currently renting could end up spending less by buying, with this likely to support prices over the coming period.

A lot can happen over the next 10 years. If home prices grow by more than we expect, many more homes will be financially beneficial to buy rather than rent.

This analysis can also not encapsulate all of the costs and benefits of buying and renting. Many like to own their home so they can make modifications, both cosmetic and structural. Owning can also provide more security of tenure; having to move is a constant concern for many renters.

But renting has benefits too: it is easier and cheaper to move to a new location or larger home for renters.

This analysis provides a comprehensive financial starting point for those deciding whether to buy or rent. But the decision, while based in finances, is also emotional.